Buying or selling items online. Sending money to a loved one overseas. Putting down a security deposit on a new apartment. These situations all have one thing in common: They’ve got the potential to put your money at risk.

As much as we love the freedom of cash, there are times when you need a payment method that’s a little more secure. And sometimes cutting a personal check isn’t enough. That’s when a money order comes in.

But what is a money order? And when is it a good idea to use one?

What Is a Money Order?

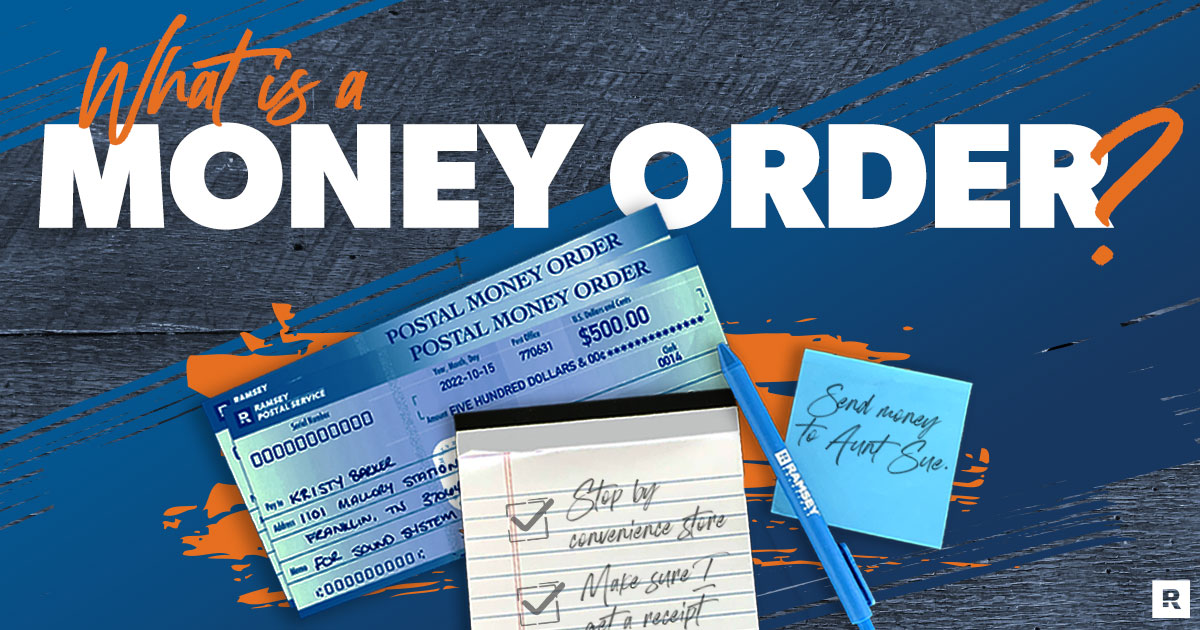

A money order is basically a prepaid check.

Let’s say you’re buying your cousin’s old sound system for $500. You can go to a business that sells money orders—like a grocery store, pharmacy or post office—and buy a $500 money order. They’ll print it out with all the right details, including your name, who it’s for and the amount.

After that, you’ll give the money order to your cousin. He’ll give you the sound system. And then he’ll take the money order to the bank and either cash it or deposit it, just like a check. It’s that easy!

The money order helps the sale go smoothly because it’s prepaid, so your cousin knows you actually have the money. And it helps protect you too (more on that in a minute).

Just make sure you buy your money order with cash or a debit card—no credit cards. Charging it to a credit card is basically like taking out a loan: You get something with real cash value and say you’ll pay it back. But for all the business knows, you might not.

That’s why most businesses won’t actually accept credit cards as payment for money orders. And the ones that do will charge you extra fees to try to make up for the risk they’re taking on.

In other words, just pay up front with cash or debit.

How Much Is a Money Order?

Whenever you buy a money order, you’ll pay the business a processing fee. That’s how they make money on these things . . . but not a lot money. Post offices and stores charge less than $2 per money order.1 And some stores, like Walmart, charge less than $1.2

But buyer beware—you can expect to rack up way more fees if you buy from a bank. Most banks charge about $5 per money order. And if you use them regularly, those repeat fees add up.

So basically, the bank is charging you more than double what other locations are for the “privilege” of sending your money somewhere outside their building. This is just another way they use outrageous fees to suck the life out of their own customers.

The best thing to do is shop wisely and purchase your money order from a store or post office instead.

Also, keep in mind that there’s a $1,000 limit for a money order (or $700 for international money orders), but you can always get multiple money orders if you need to pay for something over $1,000.3

Where Can I Get a Money Order?

Luckily, you don’t have to go out of your way to get a money order, because you can buy them at places where you’re probably already running errands. As we said earlier, one of the most popular places to get them is at the post office. Many big-box retailers (like Walmart) sell money orders, and so do most grocery stores, including Kroger, Publix and Safeway.

Budget every dollar, every month. Get started with EveryDollar!

You can also get a money order from a financial agency, like your bank or a MoneyGram or Western Union. But again, you’ll likely pay the biggest fees at these locations. To save money, we suggest getting a money order at a grocery or retail store.

Money Orders vs. Cashier’s Checks

When you hear about money orders, you’ll usually hear about cashier’s checks too. The main differences are where you get them, how much they cost and how much they’re worth.

Cashier’s checks are also prepaid checks, but unlike money orders, you can buy cashier’s checks only from a financial institution like a bank or credit union.

That’s partly because cashier’s checks can be worth more money and don’t usually have an amount limit. But it’s mostly because when you buy a cashier’s check, you’re actually putting your money into the bank’s account. So when the recipient deposits the cashier’s check, the funds come out of the bank’s account, not yours.

This transfers the risk to the bank, so they use that increased risk as an excuse to charge even higher fees—around $10.

Money Orders vs. Certified Checks

Like cashier’s checks, certified checks don’t have an amount limit and can only be bought at banks and other financial institutions.

But certified checks aren’t prepaid—they come from your checking account like a personal check would. “Certified” just means someone who works at the bank looked at your account and said, “Yep, you’ve got enough money.” That way, the person receiving the check knows it won’t bounce.

The crazy part is that banks charge as much or more for certified checks than for prepaid ones! Most certified check fees run from $5 to $15, which is a ridiculous price to pay for someone taking three seconds to print and stamp a check.

The other problem is that since certified checks withdraw directly from your account, they’ve got your name and account info written on them. And that can be a really bad idea for security reasons.

Why Should I Use a Money Order?

Money orders let you send and receive large amounts of money safely without stupid bank fees. And most importantly, they help guard your personal information.

Sure, money orders will include your name and address, but unlike a personal or certified check, they won’t include your bank account or routing numbers. It’s a lot harder for people to steal your financial identity without that info.

And that’s good. You need to make identity theft as difficult as possible—because the sad truth is, thieves and scammers just can’t wait to steal your identity and money if they get even the smallest chance. That’s why identity theft protection is a must.

Every money order also comes with a receipt and a tracking number for extra security. So that way, if your cousin tries to say, “Hey, you owed me $500 and only gave me $100,” you can whip out that receipt to show that the money order was worth the full $500.

The tracking number is obviously helpful when you’re mailing a money order, especially abroad, because you can tell exactly where it is and make sure it reaches the right person. That cuts way down on the risk of someone lying about lost funds—and on the chance of an actual loss.

When Should I Use a Money Order?

Here are a few of the most common times you might need to pay with a money order:

Buying From a Private Seller

Remember, you’re not buying a $5 garden gnome at a yard sale. We’re talking about paying for bigger items—like electronics, collectors’ items or used cars—from a private seller.

Since money orders protect your banking info, you can feel safe knowing the seller can’t access your bank account or debit card info from the money order. That’s super important if you’re buying from an online seller you don’t know (or if your neighbor Joe turns out to be a huge jerk when he sells you his iMac).

Selling to a Private Buyer

When you’re the seller, you need to know the buyer can actually pay for whatever you’re selling. The last thing you want is for them to write a bad check and disappear into the sunset.

You can help prevent that by asking buyers to pay with a money order for valuable items. Since the money order is prepaid, you can feel pretty confident that they have the funds.

Sending Funds

These days, you can send money through a ton of digital payment platforms. But there are still some legit reasons to send money physically—like putting down a security deposit on a new apartment or giving funds to a family member in the military.

Mailing cash or checks can be risky. They might get stolen, lost or damaged. And that risk goes up if you’re sending money overseas because of the extra processing and travel time.

But with a money order, the tracking number lets you see where it is and when the recipient got it. And only the person whose name is on the money order can use it. So if it does get lost or stolen, it won’t do the crook any good.

Paying Debts

This one might surprise you because most people pay debts with checks or online. But if you owe a lot of money or you’re dealing with scummy collection agencies, those payment methods may actually cause more problems.

Let’s say you send the collection agency a check. Just like scammers, collection agents can use the account and routing numbers from your check to access your account. And they’ll do the same thing with your debit card (which is why you should never give collectors debit card access).

Even if you said they could only take $100, most of these companies don’t listen. They’ll take the money you planned to use for the house payment, the utility bill and the kids’ clothes. They don’t care about your family—they just want their money.

What’s really wild is that most banks will not only let this happen but also charge you overdraft and low balance fees after the collectors drain your account. Talk about kicking you while you’re down!

If you can’t count on your bank to protect you, you may have to take matters into your own hands and pay your debt with a money order.

Collectors can’t use money orders to access your account, so you can pay what you’re truly able to—not what they’re trying to scare you into paying. When you’re behind on a lot of bills, you may have trouble catching up because you’re not sure how much you can afford to pay on each one. If that’s you, start with these steps to get back on your feet.

The important thing is, you’re still paying what you owe. You’re just protecting your accounts and identity from crummy collectors while you do it.

Avoiding Money Order Scams

As great as money orders are at protecting your identity, you still need to use good judgment and watch out for scams, like counterfeit money orders. And you have to be on your guard because your bank won’t catch these scams for you. That’s right—these financial pros can’t recognize a money order scam when they see one.

They’ll let you deposit a fake money order and spend the “funds.” Then, when they realize those funds never existed, they’ll make you pay back what you spent. And if that wipes out your account, that’s not their problem. In fact, they’ll charge you fees for overdrawing your account.

So, not only will your bank leave you on the hook for a scam you both fell for, but they’ll also put salt on the wound by charging you for it. Isn’t that crazy?

And if you think you won’t find yourself in this situation with your bank, think again. Fake checks—including money orders—are more common than you might realize. The Federal Trade Commission’s Consumer Sentinel Network database shows that close to 37,000 fake checks were reported in 2021.4

The good news is that you can take steps to protect yourself, like calling the business that issued the money order—MoneyGram, Western Union and so on—to verify that it’s legit.

You should also make sure you trust the person you’re working with. If you’ve got a bad feeeeeling (as we call it in the South), you’re probably right. Trust your gut and keep asking questions until you’re sure the money order is real.

Bank on Your Budget

The best way to control your money is with a budget. Sign up for EveryDollar and start today--for free!

Sign Up

Did you find this article helpful? Share it!

About the author

Ramsey