What Are the Different Types of Bankruptcies?

13 Min Read | Nov 17, 2023

Okay, guys. So you’re sitting at the kitchen table, staring down collection notices and wondering how you’re going to make things work. Maybe you’ve recently lost your job and the debt is piling up to an overwhelming amount. And then you think it—that word you never thought you’d have to consider: bankruptcy.

I know from experience. Sometimes your situation seems so hopeless that bankruptcy looks like your only option. I know you might feel scared and backed into a corner, but bankruptcy isn’t a decision to make lightly. It’s important to know exactly what bankruptcy is and what the different types of bankruptcies are so you can make the best decision for your situation.

What Is Bankruptcy?

You probably came across the word “bankruptcy" playing a game of Monopoly or watching someone on Wheel of Fortune lose all their money on a bad spin. But in real life, bankruptcy is a lot more serious: It’s when you go before a judge and tell them you can’t pay your debts. Then, depending on the situation, they either take everything in exchange for erasing your debts or allow you to keep your stuff as long as you make a plan to pay them back.

People file for bankruptcy for a few reasons—like the fallout from a job loss, a divorce, a medical emergency or a death in the family. In fact, more than 730,000 nonbusiness bankruptcies were filed in 2018.1 Holy crap!

Real talk: Bankruptcy is a major life event that affects more than just your finances. It can follow you when you’re trying to apply for a job, buy a house, or start a business. Even though people might see it as a “fresh start,” bankruptcy only treats the symptoms, not the behaviors that led to your money problems.

And you’ve got to remember that bankruptcy doesn’t clear student loans, government debts (taxes, fines or penalties), reaffirmed debt (where you recommit to the terms of a current loan), child support or alimony. So, if those are your only debts, bankruptcy won’t clear them.

What Are the Types of Bankruptcies?

Even though the general goal of bankruptcy is to clear debt, not all bankruptcies are created equal. In fact, there are six different types of bankruptcies:

-

Chapter 7: Liquidation

-

Chapter 13: Repayment Plan

-

Chapter 11: Large Reorganization

-

Chapter 12: Family Farmers

-

Chapter 15: Used in Foreign Cases

-

Chapter 9: Municipalities

You may have just taken one look at this list and zoned out for a second. That’s okay. More than likely, you’d only be dealing with the two most common types of bankruptcies for individuals: Chapter 7 and Chapter 13. (A chapter just refers to the specific section of the U.S. Bankruptcy Code where the law is found.2) But we’ll take a look at each type so you’re familiar with the options. Let’s go!

Chapter 7 Bankruptcy

Also known as liquidation or straight bankruptcy, Chapter 7 is the most common type of bankruptcy for individuals. A court-appointed trustee oversees the liquidation (sale) of your assets (anything you own that has value) to pay off your creditors (the people you owe money to). Any leftover unsecured debt (like credit cards or medical bills) is typically erased. But as I mentioned earlier, this doesn’t include debts that aren’t forgiven through bankruptcy, like student loans and taxes. So if you thought this was your loophole to get out of those student loans, think again.

Get help with your money questions. Talk to a Financial Coach today!

Now, depending on which state you live in, there are some things the court won’t force you to sell. For example, most people can hold on to basic necessities like their house, car and retirement accounts during Chapter 7 bankruptcy, but nothing is guaranteed. Chapter 7 also can’t stop a foreclosure—it can only postpone it. The only way to keep the stuff you still owe money on is to reaffirm the debt, which means you recommit to the loan agreement and continue making payments. But most Chapter 7 bankruptcies are no-asset cases, which means there’s no property with enough value to sell.

You can only file for Chapter 7 bankruptcy if the court decides you don’t make enough money to pay back your debt. This decision is based on the means test, which compares your income to the state average and looks at your finances to see if you have the disposable income (aka the means) to pay back a decent amount of what you owe to creditors. If your income is too low to do so, then you may qualify for Chapter 7.

Keep in mind if you file for Chapter 7 bankruptcy, you’ll have to attend a meeting of the creditors where people you owe money to can ask you all kinds of questions about your debt and your finances.

Um, no thank you. Y’all already harass me nonstop—now you want to depose me? I’d rather pay off my debt than give them the satisfaction.

A Chapter 7 bankruptcy also follows you around like a bad smell. Or worse, it’s as if every day you had to wear a white shirt with a giant ketchup stain on the front. It’s a giant red stain (and stench) on your credit report for the next 10 years. That’s like an eternity when you think of all you could accomplish financially on your own in 10 years. And not that you ever should, but just know, you won’t be able to file for bankruptcy again until eight years pass.

Chapter 13 Bankruptcy

While Chapter 7 bankruptcy often forgives your debt, Chapter 13 bankruptcy basically reorganizes it. The court approves a monthly payment plan so you can pay back a portion of your unsecured debt and all of your secured debt over a period of three to five years. The monthly payment amounts depend on your income and the amount of debt you have. But the court also gets to put you on a strict budget and check all your spending.

Now, this is a trip to me—especially since I see people get on a budget and pay off all of their debt on their own in 12–24 months, on average. Then they go on to save 3–6 months of savings. Why have someone force you to budget when you can control your spending yourself?

Unlike Chapter 7, this kind of bankruptcy allows you to keep your assets and catch up on any debt that isn’t bankruptable. (Is that a word? I’m going with it.) Chapter 13 can also stop a foreclosure by giving you time to bring your mortgage up to date.

Anyone can file for Chapter 13 bankruptcy as long as their unsecured debt is less than $419,275 and their secured debt is less than $1,257,850.3 Plus, you have to be up to date on any tax filings. You should also know that a Chapter 13 bankruptcy stays on your credit report for seven years, and you can’t file for it again for two years.

Chapter 11 Bankruptcy

For the most part, Chapter 11 bankruptcy is used to reorganize a business or corporation. Businesses come up with a plan for how they’ll continue operating the company while paying off their debt, and both the court and the creditors must approve this plan. Some individuals, such as real estate investors, who have too much debt to qualify for Chapter 13, but who also have a lot of high-value properties and assets, may also choose to file under Chapter 11. But unless you’re a pro athlete or a celebrity, you’re probably not going to mess with this one.

Chapter 12 Bankruptcy

This is a repayment plan that allows family farmers and fishermen to avoid having to sell all their stuff or foreclose on their property. While it’s similar to Chapter 13 bankruptcy, Chapter 12 is a little more flexible and has higher debt limits.

Chapter 15 Bankruptcy

Chapter 15 deals with international bankruptcy issues and gives foreign debtors access to U.S. bankruptcy courts.

Chapter 9 Bankruptcy

Chapter 9 bankruptcy is another repayment plan that allows towns, cities, school districts, etc. to reorganize and pay back what they owe.

For more specific information about bankruptcy laws in your area, visit the United States Courts website.

Which Type of Bankruptcy Is Right for My Situation?

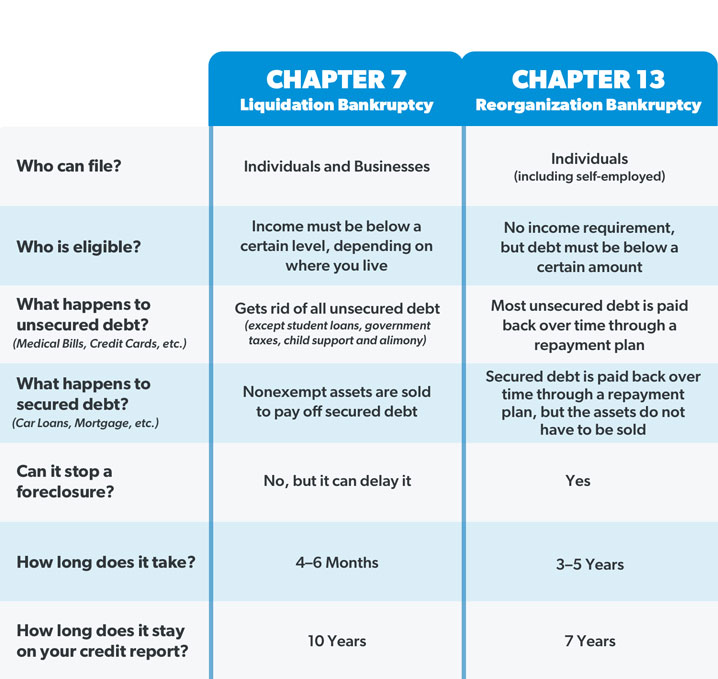

Since the other types of bankruptcies are specifically geared toward certain individuals or businesses, most people only qualify for Chapter 7 or Chapter 13. Here’s a side-by-side comparison to show how they’re different:

The biggest difference between Chapter 7 and Chapter 13 bankruptcy comes down to the person’s assets and income level. For instance, if someone had a recent job loss or an unsteady income, they might fall into a Chapter 7 bankruptcy. But if the means test says they make enough money to pay back their debts, they would fall into a Chapter 13 instead. Someone might also apply for Chapter 13 if avoiding home foreclosure is a top priority, or they could go for Chapter 7 if timing is an issue—since it’s significantly faster than Chapter 13.

But bankruptcy is a nerve-wracking experience, and choosing between Chapter 7 and Chapter 13 is like trying to pick the lesser of two evils. In both cases, privacy goes out the window. All your information literally gets laid out on a table for the court to look through. Then there’s the fact that about half of Chapter 13 bankruptcy cases nationwide are dismissed because the debtor can’t make the monthly payments.4

And while creditors are not legally able to hound you for money while you go through the bankruptcy process, the court will come after you harder than any credit card company can if you miss a payment in Chapter 13. But if your case is dismissed, then creditors can take their cut directly from your paycheck and your home might go into foreclosure. Is it just me or does bankruptcy seem scarier and less controllable than learning how to get your money under control for yourself?

Bankruptcy may seem like a magic wand that can make all your problems disappear. But to quote Talladega Nights, “Don’t you put that evil on me, Ricky Bobby!” I’m steering clear of bankruptcy at all costs because it also takes a huge emotional toll.

I’m sure you’ve heard of financial guru Dave Ramsey. Well, before he got guru status, my guy Dave walked through bankruptcy himself. It was such a painful process that he completely changed the way he handled money and developed a plan (aka the Baby Steps) to help others do the same. Well, Dave never advises anyone to consider bankruptcy. In fact, he says bankruptcy falls into the same category as divorce—it should only be your last resort, after you’ve tried every other possible route first.

So, let’s look at some ways you can avoid filing for bankruptcy altogether.

What Are Some Alternatives to Filing for Bankruptcy?

Please believe—no matter how deeply in debt you are—it is possible to avoid bankruptcy. Take it from me, someone who paid off almost half a million of consumer debt. I know what’s possible out here. You just need to know your options. Here are a few steps you can take that will help get you out of debt without filing for bankruptcy.

Take care of necessities first.

Before you do anything, you want to make sure you’ve got food, utilities, shelter and transportation covered. At Ramsey, we call these the Four Walls. You won’t have the energy to fight your way out of debt if you don’t have a house to sleep in or food to eat. So, make sure you’re taking care of yourself and your family first. The bill collectors can wait.

Don't Go It Alone: Connect With a Financial Coach

A trained financial coach helps you navigate your money problems and make real money progress.

Get on a budget.

I mentioned before that in Chapter 13 bankruptcy, the court puts you on a budget and tracks your spending. But the truth is, you can do those things on your own, without filing for bankruptcy. If you’re on your last leg, making a budget can be a total game changer. By tracking where your money is going—instead of wondering where it went—you’ll find money you didn’t even realize you had.

And yeah, budgeting also means cutting all unnecessary expenses to pay off debt. The cable and the subscriptions have to go! No more eating out. No more vacations. We’re talking survival mode, y’all. But instead of the government telling you how to manage your money for five years in a bankruptcy case, you get to call the shots.

Boost your income.

Your income is your most powerful wealth-building (and debt-fighting) tool. The more money you make, the more you can throw at your debt. When I set out to pay off my debt with my husband, our income was not it. So we had to do things to increase it. And you probably do as well.

You may need to pick up a second job or work more hours at your current job to help keep you afloat while you catch up on those monthly payments. Yes, it can be exhausting, but your temporary sacrifice will be worth it in the long run.

Sell your stuff.

Remember how we said the court liquidates your assets in Chapter 7 bankruptcy? What if you sold your stuff instead? If you’ve got anything of value, like boats, fancy lawn mowers or anything with a motor that you don’t use to drive to work, sell it! Furniture, collectibles, jewelry, that guitar you promised to learn to play someday—anything you don’t need has got to go.

Sound extreme? This is basically what could happen if you file for bankruptcy—except you wouldn’t have control over how your things get sold. So, hit up Craigslist, eBay and Facebook Marketplace and turn your stuff into fast cash. And trust me, it will feel a lot better when it’s on your terms.

Back in the day, we sold everything in our house that wasn’t an absolute necessity. We even sold our furniture. But let me tell you—sleeping on an air mattress was easily worth it to be debt-free.

Work with a coach.

Speaking of worth it, there’s one thing you probably haven’t tried yet but can make all the difference: working with a coach.

Right now, bankruptcy may look like the biggest thing in your life, but it doesn’t get to say who you are or what your future will be. You have what it takes—especially with a Ramsey Preferred Coach (RPC) in your corner. Book a free consult with your RPC today.

Did you find this article helpful? Share it!

About the author

Jade Warshaw