Personal finance can seem super intimidating—after all, it covers all the decisions you make with your money throughout your life. But trust us, it doesn’t have to be complicated!

When you break it down, you’ll see the basics of personal finance are actually very manageable steps you can and will get a handle on. So, let’s get started.

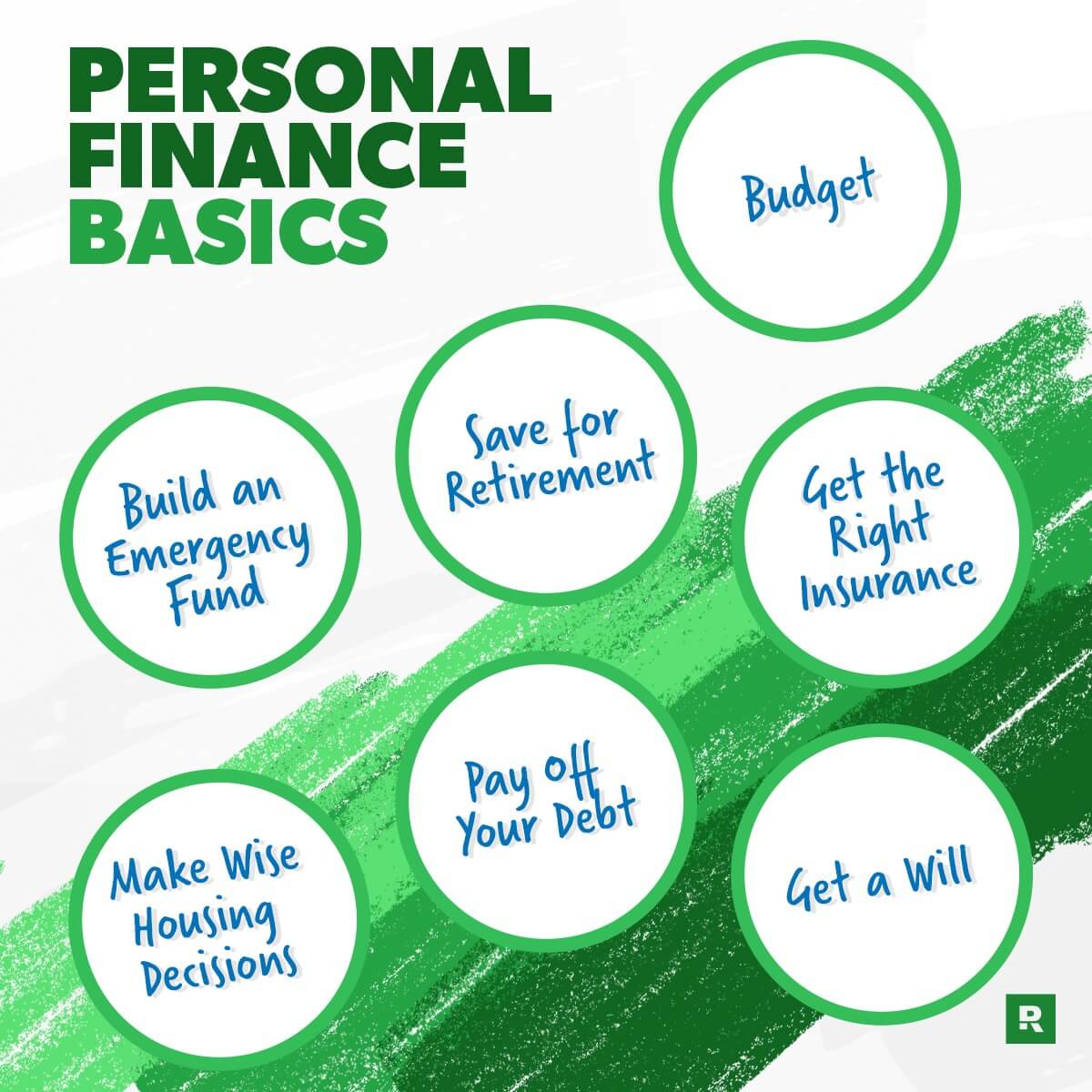

Create a Budget

To start, you need to create a budget. Why? Budgeting is the foundation you’ll build all the rest of your personal finance habits on top of. That’s because budgeting, plain and simple, is making a plan for your money—every dollar coming in and every dollar going out. Here’s how to do that.

- First, list your income. Income is any money you plan to receive during that month. That includes take-home pay and any side hustle money.

- Next, you’ll subtract all your expenses. Start with giving and saving, and then plan for your Four Walls: food, utilities, shelter and transportation. After that, list your common monthly expenses like insurance and childcare. If there’s still money left, list out extras like eating out and entertainment.

If you have money left when you’ve subtracted all your expenses, give yourself a high five. But don’t leave that money as “extra.” Put it to work toward your current money goal, like saving or paying off debt.

If you end up with a negative number, you need to cut expenses until your income minus your expenses equals zero.

- The next step for budgeting is this: Track your expenses (which, by the way, is one of our top personal finance tips, period). Do it all month long. This means any money that goes in or out of your bank account needs to be tracked in your budget—into the right budget line.

This is how you stay on top of your spending, keep from overspending, and get real with your money habits. Because your budget is the plan, and tracking is the accountability.

- Finally, create a new budget each month (before the month begins). Remember to get in any month-specific expenses so you’re ready for what’s coming your way.

If you want some more info on how to start, play around with our Budget Calculator.

Save for Large Purchases or Semiannual Expenses

Not every expense in your life happens on a regular, monthly routine. You should use a sinking fund to save up for these bit by bit, like if . . .

- Your car tires are beginning to wear thin—start saving for replacements.

- You’ve got an insurance premium that’s due twice a year—divide the cost and save part of the total each month.

- You have an annual membership to something—again, divide the cost and save some each month.

- You want to work on home repairs or buy new furniture—save up until you can pay in full.

A sinking fund is a great way to save up for large and semiannual expenses because you can budget for them over time to spread out the cost. That way, your budget isn’t blindsided by something you knew was coming up.

Build an Emergency Fund

Your grandmother told you to save for a rainy day. Why? Because. It. Rains. She called it a rainy day fund—we call it an emergency fund.

Begin with a $1,000 starter fund. Then once you’ve paid off all your debt (more on that later), use that extra cash you were spending on debt payments to build your fully funded emergency fund. Here’s how.

First, look at your budget. How much does it take to keep your household running each month? If your income went away, what essential bills and obligations would you still have to meet?

Start budgeting with EveryDollar today!

You want to save enough to cover 3–6 months of those expenses in case of an emergency. (That’s three months if you’ve got a two-income household and six months if you’ve got one income.)

Keep this money liquid, aka make sure it’s available. Your emergency fund isn’t a long-term investment—it’s insurance. And it needs to be at the ready if you need it. But this doesn’t mean you stuff it in between your mattress and box spring. (That’s a little too available.)

Instead, stash that cash into a simple money market account so you can get to it by writing a check or going to an ATM. That way, it’s not sitting there with your regular money as a temptation when summer vacay comes around. (That’s not an emergency, just to be clear—no matter how much you crave salty air.)

With your fully funded emergency fund in place, you’ll be ready for whatever comes your way. That kind of personal finance security will help you rest better than any seaside nap.

Save for Retirement

Retirement investing isn’t as complicated as you might think. First, let’s talk about how much to invest. When you follow the Baby Steps, you’ll start socking away 15% of your income for retirement once you’ve paid off all your debt and saved up that fully funded emergency fund we just talked about. (This is Baby Step 4.)

When you’re at that point, here’s how you jump in: See if your employer offers a 401(k) or 403(b) with a match. If they do, invest in your 401(k) up to the employer match to take advantage of that free money!

If you already have a traditional 401(k) through work (meaning you fund it with pretax money), the next move is to open a Roth IRA—which you fund with after-tax dollars, allowing your growth and withdrawals down the road to be tax-free!

But since the Roth gives you such a big tax advantage, Uncle Sam puts a cap on it: You can only invest $6,500 in 2023 (or $7,500 if you’re 50 or older).1 If you max that out and still haven’t hit 15%, go back to your 401(k) and keep investing your money there.

Inside both the 401(k) and Roth IRA, you’ll want your money spread across the four kinds of mutual funds: growth, growth and income, aggressive growth, and international.

That way, you’re not investing your entire nest egg into one basket. This is what the investing world calls diversification, and it’s less risky and just plain wise.

If you’re trying to figure out how much money you need saved to retire on your terms, check out our R:IQ retirement assessment. It does the math for you and shows you exactly how much money to invest each month based on your age, income and retirement lifestyle goals.

Get the Right Insurance

Insurance is so fun, right? Right? Okay—maybe not for most of us. But that doesn’t make it any less essential. And maybe you know you’re supposed to get insurance, but you don't really know what kind or how much or with who.

Don’t you worry. Here’s a super quick rundown of the eight types of insurance you need:

- Term Life Insurance: Life insurance is all about protection and security for your family. You need a 15- or 20-year term life insurance policy. Average term life insurance rates are most often cheaper than whole life insurance rates. Plus, term life isn’t a total rip-off like whole life, which dresses up like an investment policy but has a sucky rate of return. (No, thank you.)

- Auto Insurance: Generally, for the most useful car insurance, you need full coverage, which includes liability, collision and comprehensive. If you’ve got an older, paid-for car, you can think about dropping collision. There are a few other optional types and other add-ons your state may require you to get. It’s a good idea to talk to an independent insurance agent to go over your options and get the best rates.

- Homeowners or Renters Insurance: If you’re a homeowner, make sure you have extended dwelling coverage and talk to your insurance agent about flood and earthquake coverage. Renters, your landlord is not responsible for replacing your stuff if it’s lost in a fire, burglary or other disaster. That’s why you need renters insurance to cover the cost of replacing your things!

- Health Insurance: One major medical emergency can literally bankrupt you if you don’t have health insurance. But if you’re worried about the cost, consider a high-deductible health insurance plan combined with a Health Savings Account (HSA). This is a great way to protect yourself in an emergency without paying a crazy-high premium each month.

- Long-Term Disability Insurance: Get yourself long-term disability insurance that will help replace your income if you’re no longer able to work because of sickness or injury. We recommend getting as much coverage as you can—around 60–70% of your income. You don’t need short-term disability. (Your fully funded emergency fund will cover you there.)

- Long-Term Care Insurance: If you end up needing long-term care in your golden years, don’t expect Medicare to take care of you. So when you turn 60, plan to get long-term care insurance that covers in-home care (not just nursing homes).

- Identity Theft Protection: Listen: Identity theft can happen to anyone and can take years to clean up on your own. You need identity theft protection! Make sure you get a plan that offers both protection and recovery services. You need Social Security number monitoring, change of address monitoring, recovery services and reimbursement. That means someone else will plug in all those hours to get your life back in order when you need it!

- Umbrella Insurance: If your net worth is over $500,000, you need umbrella insurance to protect your home and savings from liability lawsuits that exceed your home and auto insurance coverage. Not fun to think about, but necessary!

Phew, that’s a lot. But don’t worry: You don't have to be an insurance expert to be well insured. (Thank goodness!)

But you do have to be proactive. Try our 5-Minute Coverage Checkup. It's easy, quick and clear—three of our favorite words in this hustle-and-bustle world. Plus, you might even save some cash—three more of our favorite words!

Get a Will

We’re just going to come out and say it: You need a will. It’s part of getting your personal finances in order and part of being a responsible adult—not a fun part, but an important part.

You don’t want the government to decide what happens to your stuff, your money or your family (which is exactly what will happen if you don’t take charge here).

Yes, it’s a lot to deal with—making huge decisions about something you don’t really want to think about in the first place. But listen, you need a will.

Find yourself an affordable, vetted online provider who cuts the legal jargon and simplifies the process. (By simple, we mean do-the-paper-work-in-your-pajamas simple.) So, don’t put it off. Get a will today.

Pay Off Your Debt

Some people think debt is a tool to build credit or get fancy airline miles. The truth is, debt is a weight that presses you down and holds you back. Our own research shows that one in five Americans have fallen deeper into debt since June of 2022, and only 24% said they reduced their debt.

And unfortunately, debt and stress go hand in hand. That could be because debt keeps you from ever getting ahead. It holds part of your paycheck hostage every month with payments for something you bought months or even years ago. You don’t need that kind of stress!

Here’s a massively important personal finance tip: Your income is your greatest wealth-building tool. When you pay off your debt, you take back your paycheck. You get back those extra payments you were making toward debt.

What could you do with that extra money? Use it for extra room in the budget. Use it to move forward with your money goals, like savings and your retirement! Use it for you.

To summarize: Debt is not a tool. Your income is. Take. It. Back.

Make Wise Housing Decisions

We could make this one really complicated. But that’s not our thing. Our thing is making personal finance clear and simple.

So, here are the three main points you need to remember when you’re thinking about buying a house.

- Don’t spend more than 25% of your monthly take-home pay on housing costs. If you get a mortgage, that means your monthly payment, PMI, property taxes, insurance and any HOA fees combined shouldn’t be more than 25%. (The same rule applies to renters—your rent and any other fees connected shouldn’t be more than 25%.)

- Choose a 15-year fixed-rate conventional loan if you’re going to get a mortgage. (You’ll literally save thousands overall compared to expensive FHA, VA and 30-year loans.)

- Save at least 20% of the home’s cost for a down payment to avoid PMI fees before you buy a house.(First-time buyers can save a smaller down payment like 5–10%—but then you will get stuck with PMI.)

Without following those three guidelines, you can quickly become house poor—meaning your house might be awesome, but it takes up so much of your income that you struggle financially in other areas.

Get a Game Plan for Your Money

So, yeah, personal finance is a lot. But you can make better decisions with your money—big and small. You just need the right game plan.

With Financial Peace University (FPU), you’ll learn everything you need to know about managing your money well. From creating a budget and paying off debt to saving for emergencies and investing for the future, this course will walk you through all the basics of personal finance (without the confusing financial blah blah blah everyone else is dishing out).

Ready to start learning? Go watch FPU now!

Did you find this article helpful? Share it!

About the author

Ramsey