Your workplace retirement plan—a 401(k) for most of us—is the foundation of a solid retirement plan. The employer match alone means you get an instant 100% return on at least part of the money you put into your 401(k). That’s why Dave recommends you start your retirement investing with your 401(k) by investing enough to receive the full employer match.

But that’s not all. Your 401(k) also has some tax benefits:

- Your pretax 401(k) contributions lower your taxable income, making it easier to invest more.

- The growth of your 401(k) is also tax-deferred, which means your money grows faster.

All that is great, but it won’t be enough for most people. Once you’re getting the full employer match on your 401(k), your next step is to invest in a Roth IRA, which has several positive points of its own.

Tax-Free Withdrawals Help Your Roth Live Longer

Your 401(k)’s tax-deferral works in your favor while you’re investing, but when you retire, you’ll have to pay taxes on the money you withdraw. However, you’ll fund your Roth IRA with after-tax money, and it also grows tax-free. That means you won’t have to pay taxes on the money you withdraw from your Roth IRA in retirement.

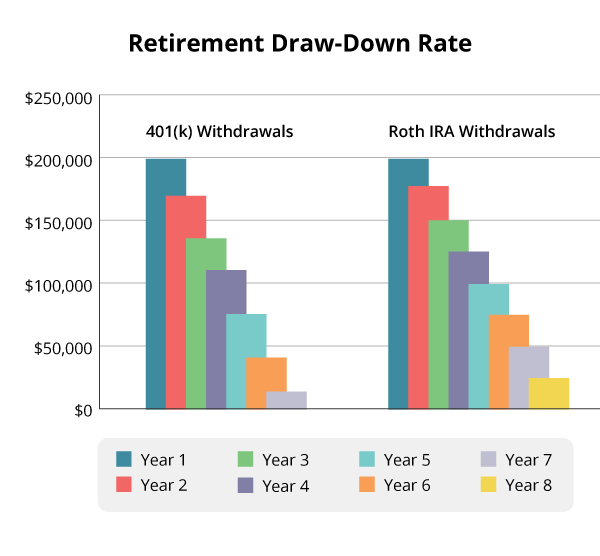

Here’s an example of how taxes can limit the life-span of your retirement account. Say your 401(k) and your Roth IRA both have $200,000 balances. You withdraw $25,000 from each for a $50,000 annual income in retirement. We’ll assume your income puts you in the 25% tax bracket, and for ease of calculation, we’ll also assume no additional growth after you retire.

You’ll actually have to withdraw $31,250 from your 401(k) to cover your taxes and still give you the income you need. By year six, you’d only have $12,500 left in your 401(k). Your Roth IRA, on the other hand, would hold out until year eight.

All you uber-nerds out there are probably pulling your hair out at how simplified this calculation is, but we don’t have to get super-technical to get this point across: Taxes will have an effect on how long your nest egg will last. That makes a tax-free Roth IRA a must-have for a secure retirement.

A Wider Selection of Funds Can Spur Growth

While your 401(k) plan offers a limited selection of mutual funds, you can choose any of the thousands of existing mutual funds for your Roth IRA. That means you can select the best of the best growth stock mutual funds to build what the investing experts call a “well-diversified portfolio” to grow your retirement nest egg.

That might not sound like a big deal, but investing studies have shown that aside from increasing the amount you invest for retirement, selecting a balanced mix of funds has the largest impact on how much your retirement account will grow—up to 38% in one study. Your Roth IRA gives you the freedom to choose the same balanced mix Dave uses for his retirement: 25% growth, 25% aggressive growth, 25% growth and income and 25% international.

Striking the Balance With Two Accounts

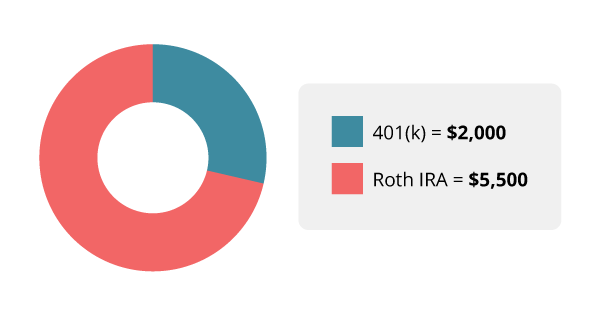

Investing in two retirement accounts isn’t complicated. You just have to do some quick math. Your initial goal in Baby Step 4 is to invest 15% of your income for retirement. That’s $7,500 for the average $50,000 annual income. If your employer matches contributions up to 4% of your pay, you’ll contribute $2,000 to your 401(k). The remaining $5,500 will go into your Roth IRA.

Some What-Ifs:

- What if my employer doesn’t offer a retirement plan or doesn’t match contributions? Max out your Roth IRA first. If you still have money to invest, you can invest in your company plan if available or open a taxable brokerage account.

- What if I max out my Roth IRA and still haven’t met my 15% goal? Go back to your 401(k) and invest the remainder to take advantage of your 401(k)’s tax deferral.

- What if my employer offers a Roth 401(k) option? Great! Dave loves Roth 401(k)s because they work almost exactly like a Roth IRA. It’s funded with after-tax dollars and grows tax-free, and you won’t have to pay taxes on the money you put in or its growth when you withdraw it in retirement. If your employer offers this option, and you have good mutual funds to choose from, you can invest your entire 15% in your Roth 401(k).

How to Get Team Roth and Team 401(k) on the Same Side

Your next challenge is to get your Roth IRA and your 401(k) to play nicely together. The investments you choose for each account should complement each other and work together to help you make the most of the stock market’s growth while limiting your risk.

Market chaos, inflation, your future—work with a pro to navigate this stuff.

An experienced investing professional can show you how to accomplish this goal and answer any questions you have about your retirement accounts. By showing your pro your entire retirement picture, you can find out if you’re on track to meet your retirement savings goal and what you can do to make your outlook even brighter.

Not sure where to start? Try this free and easy way to find an investing pro in your area.

Make an Investment Plan With a Pro

SmartVestor shows you up to five investing professionals in your area for free. No commitments, no hidden fees.

This article provides general guidelines about investing topics. Your situation may be unique. If you have questions, connect with a SmartVestor Pro. Ramsey Solutions is a paid, non-client promoter of participating Pros.

Did you find this article helpful? Share it!

About the author

Ramsey