Looking for a new ride? It’s easy to catch a case of new car fever and get googly-eyed over the latest models.

But is buying a new car really the best option? What are the pros and cons? Let’s talk about the real cost of new vs. used cars—and how to make the right choice for your budget.

Is It Better to Buy a New or Used Car?

Buying a used car is always the better choice financially. Why? Because 1) used cars are less expensive overall and 2) they don’t drop as fast in value as new cars do.

Brand-new cars lose a huge chunk of their original value in the first couple of years (even in the first hour). A used car, on the other hand, keeps more of its value over time—which means you’re not losing as much money as you do with a new vehicle.

The choice between a new or used car could be the difference between you riding the highway to wealth or spinning your wheels in a never-ending cycle of payments.

But if you’re not ready to give up on your new car dreams just yet, let’s dive a little deeper into the pros of buying a used car over a new one.

The Pros of Buying a Used Car

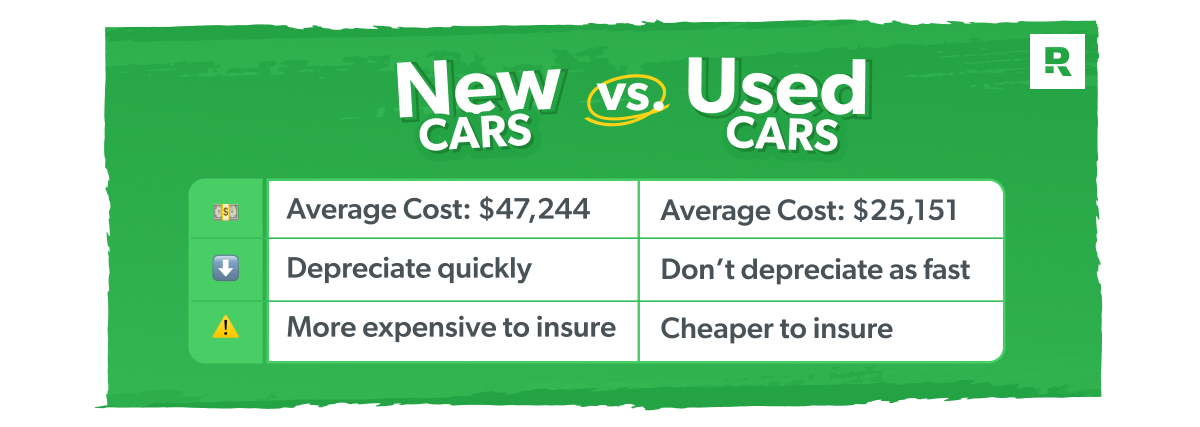

Used cars cost less.

This one may be obvious, but the price tag difference between a new car and an even slightly used one is huge.

The average transaction price for a new car is $47,244, while the average used car is listed for $25,151.1,2 That’s basically half the cost! It’s also usually easier to negotiate a better price for a used car.

But even more important is how you buy the car. And the best way to buy a car is with cash (as in, without a car loan). We know, we know. That might sound crazy, especially if you’ve always had a car payment. But a car loan is the most expensive way to buy a car!

The average interest rate is 7.18% for a new car loan and 11.93% for a used car loan.3 Any time you take out a car loan, you’re forking over thousands of dollars more—just to interest!

So, before you choose a car, figure out how much car you can actually afford.

Used cars don’t depreciate as fast.

Anything with a motor loses its value over time (this is called depreciation). But like we mentioned before, new cars lose their value much faster than used cars do—and that can make it way too easy to end up with an upside-down car loan (where you owe more than your car is worth).

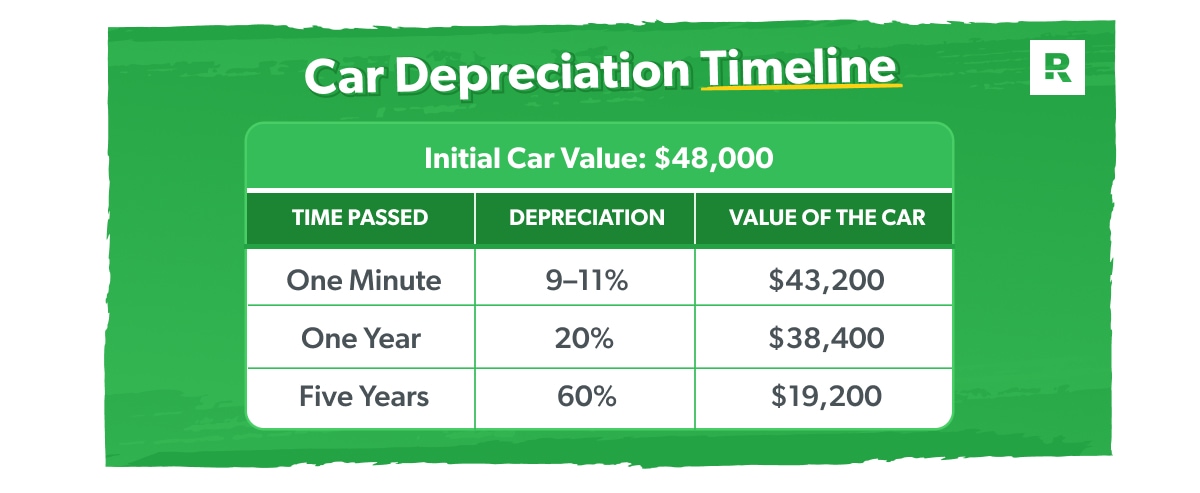

Here’s a look at how quickly a new car loses its value:

- After one minute: If you buy a shiny new $48,000 car, it loses about 9–11% of its value the moment you drive off the lot.4 You’re basically throwing $4,800 out the car window during the drive home! Ouch.

- After one year: Fast-forward 12 months and that (no-longer new) car sitting in your driveway will be worth at least 20% less than the day you bought it.5

- After five years: You can expect your car to lose around 60% of its value after you’ve driven it around for five years.6 In this case, that $48,000 car is now worth only about $19,200—if that!

Think about it: Just by choosing a car that’s a couple years old, you’re letting someone else take on the brunt of depreciation—and you’re getting a better deal!

If you buy a $48,000 shiny new car, that car loses somewhere between 9-11% of its value the moment you drive off the lot. Fast forward 12 months and that car will lose around 20% of its value from the day you bought it.

Used cars are cheaper to insure.

Not only are used cars less expensive, but they’re usually much cheaper to insure. A lot of car buyers forget to factor car insurance into the equation and then suffer from sticker shock when they see their new premium.

Don't let car insurance costs get you down! Download our checklist for easy ways to save.

The truth is, new cars cost more to repair or replace—so they cost more to insure (especially if they come with fancy extras like backup cameras and blind spot sensors). And even with some of the latest safety technology, insurance companies rarely offer discounts to new-car drivers for having those features.

New-car drivers will spend roughly $1,838 in the first year on car insurance premiums.7 But if you buy a five-year-old version of the same car, it’s 27% less to insure!8

Here's A Tip

If you’re buying a car, our RamseyTrusted insurance agents can help you find the best deals on auto coverage in your area!

New cars aren’t always more reliable.

We know safety is a big concern. And one of the most common arguments against buying a used car (especially if it’s a car for your kid) is that it’ll wear out sooner and won’t be as reliable as the new ones rolling straight off the assembly line.

But new doesn’t always mean more reliable. In fact, some newer cars (especially models in their first year of production) are among the least reliable cars you can drive.

According to J.D. Power, “New vehicles are becoming more problematic.”9 And their U.S. Initial Quality Study found a significant decline in the quality of new cars being produced, especially for vehicles with higher tech.

From faulty airbags to troublesome transmissions, many drivers of newer model cars end up making constant trips to the mechanic or getting manufacture recall notices for issues that can be serious safety hazards.

With a used car, on the other hand, you have a better idea of what to expect because it’s been on the road longer. A vehicle history report will let you know about any major repairs or potential problems. You can also search car forums and read what other drivers have to say about a certain model.

You can find used cars that are still safe and dependable—and at a much cheaper price! If you need some extra assurance, stick to brands like Toyota and Honda that have proven to be very reliable over time. Or you can narrow down you search to only certified pre-owned vehicles that have already been inspected.

Bottom line: Don’t use safety as an excuse to buy a car you can’t afford. It all depends on the type of car you’re looking at and how long the car has been on the road. Always do your research!

Cost Comparison of Buying New vs. Used

Okay, let’s break down how much you really pay for a new vs. used vehicle.

Let’s say Tony and Jack are both looking to buy new vehicles. Tony goes the “normal” route and finances a brand-new truck, while Jack decides to save up and buy a reliable used car with cash.

The average new car loan is $40,366 with a 7.18% interest rate.10 If Tony signs up for a 60-month loan, he’ll end up paying a total of $48,164 for a truck that’ll be worth about $16,000 (if he’s lucky) at the end of the loan term.

Meanwhile, Jack found a four-year-old sedan with low mileage and plenty of life left in the tank for $12,000, and he paid for it with cash. That means he owns the car free and clear. No payments!

Even if Jack has to do some minor car repairs here and there on his pre-loved ride, it’ll be nothing compared to how much Tony is shelling out toward insurance and interest every single month. And just because Tony’s truck is new, it doesn’t mean it won’t end up in the shop with its own problems.

So, what could Jack do with an extra $800 each month that he’s not using to pay off the car? Well, he could put all those savings toward upgrading his car down the road. If he saves $800 every month, he could buy a $20,000 car in about two years. Meanwhile, Tony isn’t even halfway through the loan on his truck (hope he really likes it).

Is It Ever Okay to Buy a New Car?

As a general rule of thumb, the total value of your vehicles (anything with a motor in it) should never be more than half of your annual household income. Because, again, you don’t want too much of your money tied up in things that plummet in value.

So, unless you’re a millionaire, buying a new car doesn’t make financial sense. And even then, most millionaires buy used cars!

In the largest study of millionaires, we found that the average millionaire drives a four-year-old car with 41,000 miles on it. And 8 out of 10 millionaire car buyers choose to not have a car payment.

Financing new cars is how people stay broke. So, choose used and pay in cash. You want to own your car instead of it owning you.

Save Up for the Car You Want

Whether you choose new or used, the right car is the one you pay for in cash.

We know you’re probably thinking, I don’t have that kind of money. Not yet.

Saving up for the car you want takes patience. But if you’re intentional about it, you can get a decent car faster than you think. And trust us, you’ll be so glad you went that route when you drive away in your paid-off ride, instead of being tied down to a car payment for years.

It all starts with a budget. The EveryDollar budgeting app helps you save up for big purchases—while also making sure you cover your monthly expenses. You can also see where to cut back your spending so you can put more toward your car fund.

What are you waiting for? Go ahead and create your free budget with EveryDollar today. Because the sooner you start saving, the sooner you’ll be behind the wheel of your new (to you) ride.

Save more. Spend better. Budget confidently.

Get EveryDollar: the free app that makes creating—and keeping—a budget simple. (Yes, please.)

Did you find this article helpful? Share it!

About the author

Ramsey