Every year, millions of taxpayers overpay their income taxes—and we’re not talking about pocket change. You could be missing out on hundreds or even thousands of dollars.

In 2022, the IRS sent more than 237.8 million refunds to people who had overpaid their taxes. We’re talking billions of dollars in overpaid taxes! $512 billion, to be exact.1

Many Americans make mistakes on their taxes and end up paying more than they should. If that’s you, we’ve got good news! You can reclaim your cash by filing an amended tax return.

What Is an Amended Tax Return?

An amended tax return is simply a correction to a previously filed tax return. It allows you to get back any money you overpaid because you missed a tax deduction or credit or made a math error. Hey, we can’t all be mathletes! Sidenote: If you overpaid taxes through your payroll withholdings last year, filed a correct tax return, and got a refund, you’re done. There’s no need to file another return.

The most common mistake taxpayers make is taking the standard deduction instead of itemizing deductions—or vice versa. You want to use the method that cuts your tax bill the most.

Everyone’s tax situation is different. If you can claim a big chunk of mortgage interest, real estate taxes, local income taxes, and charitable giving, you might be better off itemizing.

How to Amend a Tax Return

You might be thinking: Won’t the IRS catch any mistakes I made? Well, they might. They also might not. The IRS processes millions of returns each year. If they catch a math or clerical error while checking your return, they’ll usually correct it and you won’t need to file an amended return.

But if you have a change in your filing status, income, deductions, credits or tax liability, you’ll need to let the IRS know by filing an amended return. Maybe you found a charitable contribution statement you forgot to deduct. Or you forgot to deduct the interest on your home because you didn’t get a statement from your mortgage company.

Fair warning, though: Mistakes aren’t always in your favor. If you filed your taxes and forgot to add the $1,000 you earned from your graphic design side hustle, you’ll have to report that income on an amended return and pay taxes on it. Yes, even small amounts of income need to be reported!

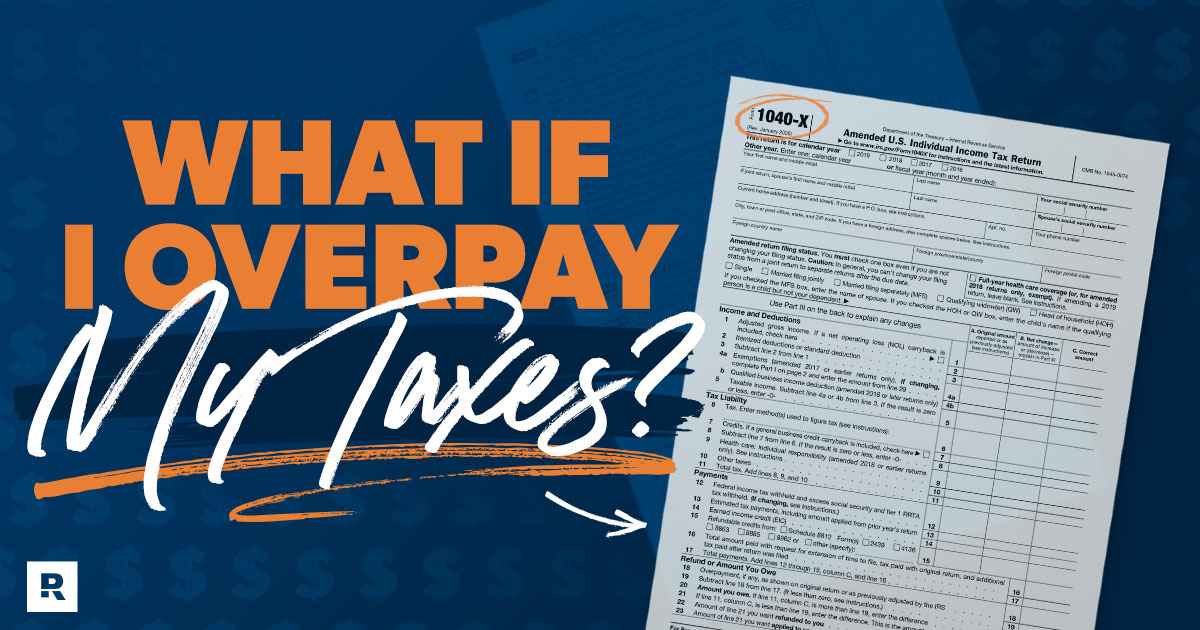

Filing an amended return is different than filling out your ordinary 1040 tax return. You’ll need to use Form 1040-X. Mark the tax year you’re correcting and explain the reason for the amendment.

The 1040-X includes three columns. Column A shows your original numbers. Column C shows your corrected numbers. And Column B shows the difference between A and C. The back of the form includes space for you to explain your changes—whether you’re owed an additional refund or have to pay additional taxes. You’ll also need to include your original 1040 form with your submission.

Amended tax returns get complicated, so you might want to hire a tax pro to help.

Keep these facts in mind if you plan to file an amended tax return:

- Generally, you must amend your return within three years of the original due date, so the oldest return you can amend is your 2019 tax return, which was due in April 2020.

- If you’re claiming an additional refund, wait until you receive your original refund to file your amended return.

- You can file an amended tax return electronically using tax software for the 2019, 2020, 2021, 2022, and 2023 tax years. Anything older than that (we’re talking to you, 2018) must be filed by paper. Yes, paper in the 21st century!

How Can I Check the Status of an Amended Tax Return?

So, you filed your amended return and are expecting to get some money back from the IRS. What’s next? Well, you wait . . . and wait . . . and wait some more. Generally, an amended return takes 16 weeks to process.2 That means it could be a sunny summer day when you submit your return and the dead of winter when you finally hear back from the IRS.

Don’t settle for tax software with hidden fees or agendas. Use one that’s on your side—Ramsey SmartTax.

If you take anything away from the process of filing an amended return (other than a refund, hopefully), it’ll be patience—and to be more careful with your taxes the next time!

You can check the IRS website to see the status of your return after three weeks. You’ll need to enter your Social Security number, date of birth and ZIP code to access the info. Then, you’ll see one of three messages: received, adjusted or completed.

The IRS specifically states not to call them for info on amended returns. But if you enjoy listening to free classical music on your phone, give them a call and wait on hold for an hour or two!

When Do I Receive a Refund for an Amended Return?

Your amended return could be delayed if it has errors, is incomplete or you forgot to sign it. (Move to the back of the line if you forgot to put your name on your paper!) You also might hear back from the IRS wanting additional information.

But if everything goes smoothly, you should get a refund check in about 16 weeks. Yes, the IRS doesn’t do direct deposits for amended returns. You’ll have to wait for an old-fashioned check in the mail.

What if the IRS Denies My Amended Return?

So, you thought Uncle Sam was going to pull out his wallet and give you some cash, but when you hear back from the IRS, it’s a no. Well, you still have options. You can file up to three amended returns—but it’s three strikes and you’re out. The IRS won’t accept any amended returns beyond three.

If the IRS rejects your return, but you think they’re wrong, you can appeal. Appeals get tricky, so you’ll probably be better off hiring a tax pro to help.

A Pro Can Help You Reclaim Your Cash

If you suspect you’ve overpaid your income taxes in past years, a tax advisor can help you discover and correct your mistakes while making sure you don’t overpay again this year. RamseyTrusted tax pros know tax code so you don’t have to. Find a tax advisor who serves your area today.

Federal Classic Includes:

- All major income types and federal forms

- Prepare, print and e-file

- Phone and email support

- 1 year of audit assistance

Federal Premium Includes:

Everything in Classic plus:

- Live chat

- Priority phone and email help

- Free financial coaching session

- 3 years of audit assistance

Did you find this article helpful? Share it!

About the author

Ramsey