There’s nothing quite like the sense of security and accomplishment when you know you’re on the path to a comfortable retirement. But that feeling can quickly dissolve into stress—even guilt—when you discover your parents are lagging dangerously behind on their own retirement journey.

"My husband and I are in a good place for retirement," Cerissa H. told us. "Our parents, however, are not—and for different reasons." Cerissa’s parents had careers in full-time ministry and never had a large income. On the other hand, her in-laws are drowning in debt thanks to several rental properties.

"We are concerned about their quality of life, the lack of long-term care insurance, and the debt," she said. "How do we prepare for a life where we will probably inherit adult dependents and debt? How do we encourage my parents to maintain hope for their financial future? And how do we respectfully talk to my in-laws about their debt?"

A Lot of Us Are Worried About Our Parents’ Retirement

It may not be much consolation, but many children of unprepared retirees are searching for answers to the same questions. The Employee Benefit Research Institute (EBRI) recently published a report on retirement and their research found the following:

- Only 50% of workers 55 and up have tried to calculate how much money they’ll need every month during retirement.1

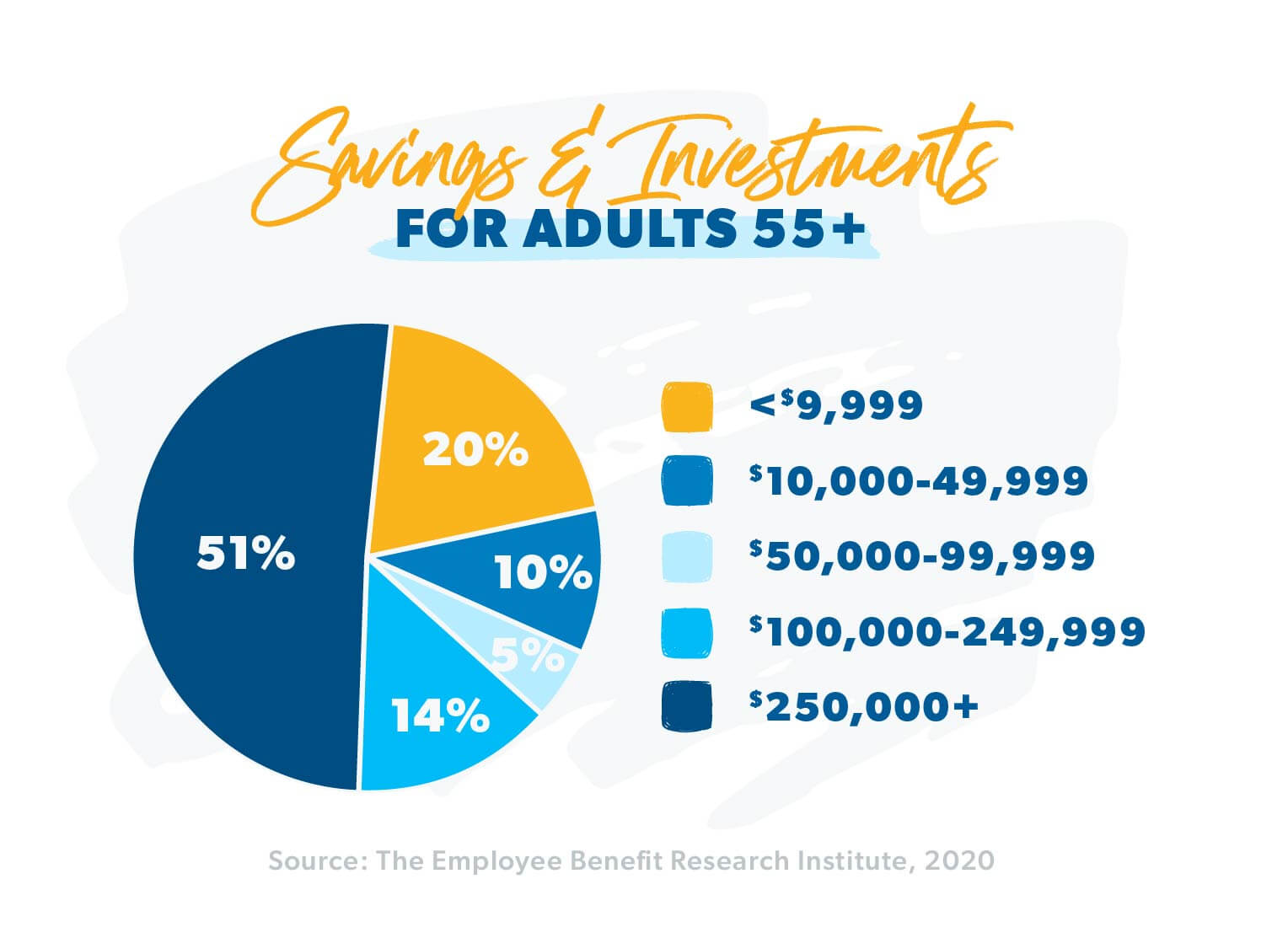

- About 1 out of 5 seniors over 55 (20%) have less than $10,000 in retirement savings.2

- Approximately 31% of seniors aren’t sure if they will have enough to cover their medical expenses during retirement. 3

- Less than half (46%) of seniors have planned for how they would cover an emergency or big expense in retirement.4

- Of retirees working for pay during retirement, 37% need the paycheck to make ends meet.5

Many adults 65 and up also have limited assets to rely on when they retire, with 21% of elderly married couples and 45% of singles depending on Social Security for 90% or more of their household income.6

Gary Shaw, an investing professional, said all of this adds up to a difficult outlook both for retirees and their children.

"I think what we’ve discovered is that parents really didn’t plan on not being able to live on Social Security," he said. "They didn’t realize their expenses, especially their health care expenses, were going to be as high as they are. Or they didn’t get their house paid off as soon as they planned, so they still have to make a house payment."

Jessica G.’s mother is almost 60 years old and has little retirement savings. Like many other seniors, she sees no other option but to keep working as long as she can. She’ll draw on Social Security to fill in the gaps of her income.

Katy C. can relate! Her mother-in-law doesn’t see herself ever retiring—often joking that her coworkers are going to have to "pry her cold, dead hands off her keyboard."

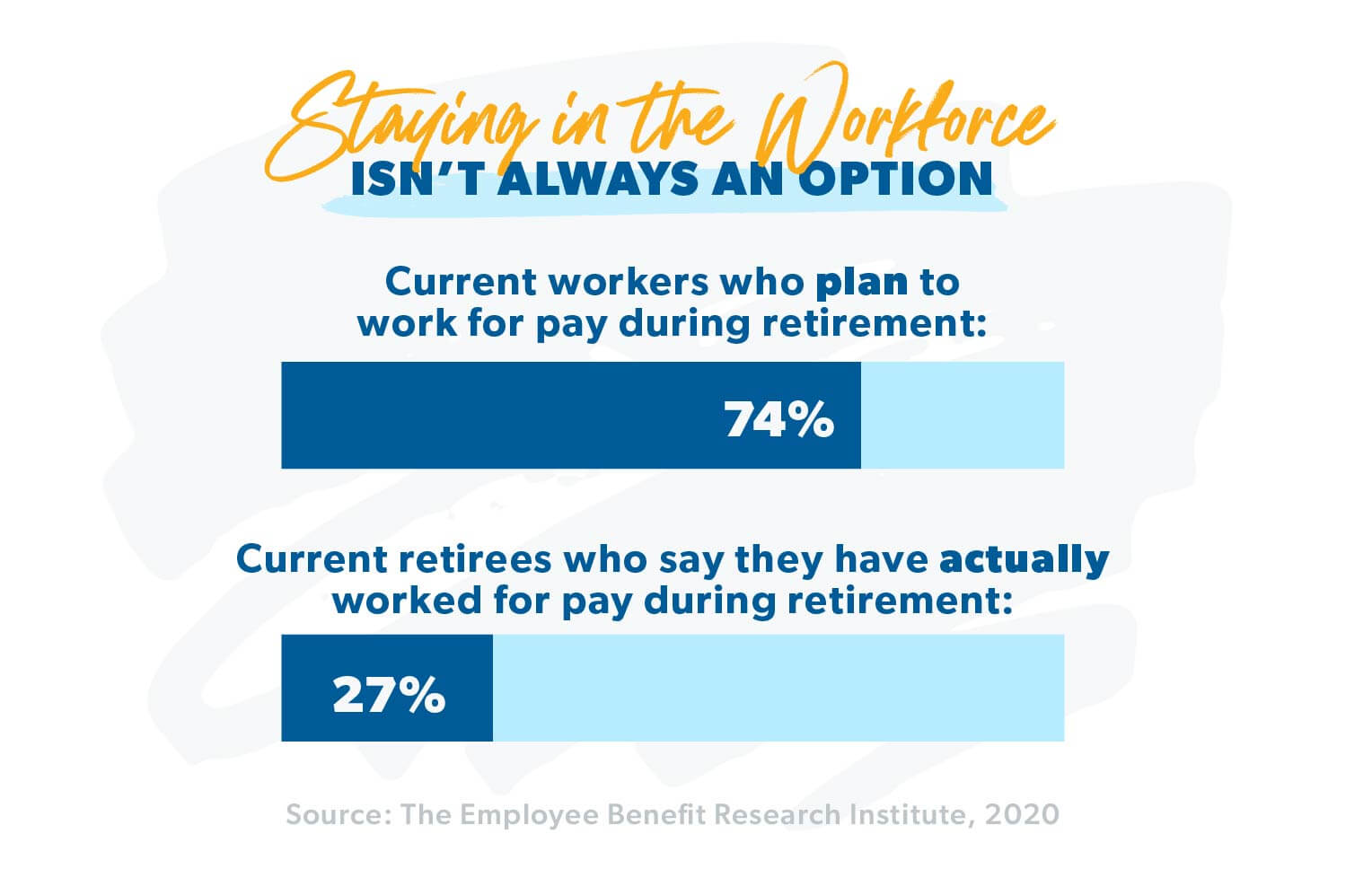

According to EBRI, Katy’s mother-in-law isn’t alone—nearly 74% of Americans plan to keep working past retirement age.7

The retirement savings crisis isn’t some problem we’re going to face many years from now—it’s already here. According to Pew Research, 10,000 baby boomers reach age 65, traditional retirement age, every day.8 But nearly half of them, 49%, have less than $10,000 saved for retirement.9 That’s not okay!

How to Start the Retirement Conversation With Your Parents

What you and your parents may have to face in the future might seem overwhelming. But don’t give up hope. It is possible to make it through this tough time with your parents’ dignity and your own retirement plans intact.

How much will you need for retirement? Find out with this free tool!

The first step is to get a clear picture of what you’re dealing with. But how do you talk to your parents about their financial situation without it being tough on everyone involved?

"Sometimes the parents won’t share all the details with the kids," Gary Shaw explained. "They don’t want them to know how bad it really is. As a parent, you want your kids to look up to you. You don’t want your kids thinking less of you because you didn’t manage money properly."

Jacob H.’s parents are struggling with that now. They’re in their mid- and late-50s and believe they have no choice but to work until they can’t anymore. They’re in debt and live paycheck to paycheck.

"I’ve tried to help them do a budget and the debt snowball," Jacob explained. "But they are very private about their money and don’t want me to see just how deep the hole is. I don’t know how to make them see that I want to help them—not just for their future, but for myself, my peace of mind, and my family."

Gary’s suggestion to avoid putting parents on the defensive is to change the tone of the conversation. Rather than focusing on what your parents are doing wrong, begin by asking how they want you, the kids, to handle their money when they no longer can.

To get the discussion started, Gary’s team uses a tool called the "family love letter" as an icebreaker. The "family love letter"—a love letter from the parents to the kids—is a document designed to make things easier when one or both of the parents are gone. It is a collection of all the important financial and medical information put into one place—the letter.

With the love letter as a guide, parents and children can cover the basics, then dig deeper into the problems as they work together to find the best possible solutions.

Retirement Talks With Your Parents Can Still Be Tough

Even with the lines of communication open, things don’t always go smoothly. Once their true retirement situation is out in the open, your mom and dad could feel very vulnerable, making them want to resist change. You may need to help them understand the need to change.

Liz A. knows what that’s like. Her mother is in deep financial trouble. She makes good money, but she’s in debt and often has to borrow from Liz and her sister to pay bills. "She will not listen to anyone about her finances," Liz says. "She gets emotional and very, very defensive."

In cases like that, Gary says it can be helpful to bring in a third party as backup.

"I had to have a tough talk with one retired couple," Gary told us. "The kids thought mom was spending too much, but they didn’t know how to tell her—so they asked me to tell her."

The kids were right. Their mom’s spending had put her and her husband in danger of running out of savings in less than three years. Gary didn’t sugarcoat the truth. He told Liz’s mom that something needed to change. Either she kept spending like she was and the money would run out far sooner than she’d ever imagined, or she could slow down on the spending and her money might stretch an additional five or even six years. A little discipline could help her go a long way!

"She got a little defensive at first, but after she let it sink in, she finally agreed she needed to stop spending so much," he said. "That was a difficult conversation to have, but it’s a fair thing to ask of your investment professional. We’re here to walk through life with you—and this is a real part of life."

Your Retirement Is Still Your Priority

You may feel it’s your duty to step in and help your parents make ends meet. You’re not alone. Jessica K. voiced the same concern: "I’m incredibly scared of having to provide for my parents once they get to retirement age. I honestly don’t know how we are going to help them while trying to build up for our own future."

Gary’s advice to Jessica and others in a similar boat? As tough as it may be, you have to focus on your own retirement plan first. Then provide whatever help you can, when you can.

"Some kids are going to feel guiltier about that than others," Gary said. "But it’s the same as when Dave says you should invest 15% for your retirement before you save anything for your kids’ college. Your financial health is what will make them financially healthy—so that’s what you need to focus on."

Gary has seen this struggle time and time again with his clients. "In one case, the daughter of the retired couple felt obligated to help her parents," he explained. "She and her husband had really good incomes and were doing great on the Baby Steps. In fact, they were on a good track to pay their own house off early."

Encouraging the couple to stick to their retirement plan, Gary advised the wife to help her parents by giving them small amounts of money to help them make ends meet. Then, as extra money became available, she could increase the amount.

"A few years down the road, they paid off their own house, and that freed up a lot more cash each month," Gary said. "She was able to increase the money she was giving to her parents on a regular basis."

By taking care of her own financial health, Gary’s client was eventually able to do more to help her parents than she would have been able to if she and her husband had sacrificed their goal of paying off their home early.

Paying off your home early, saving for retirement, being able to help loved ones—all of that can happen for you.

Protect Your Retirement With Long-Term Care Insurance

With their feet on solid financial ground, and with more money available to help the wife’s parents, Gary recommended that the couple consider buying long-term care (LTC) insurance for her parents to help cover expenses related to nursing home, in-home or assisted living care.

"It’s going to fall on them later to pick up those expenses anyway," Gary reasoned.

Another of Gary’s clients, Sandy L., experienced the financial setback of her parents not having long-term care insurance. Her mother suffered a debilitating stroke two years ago, and she now lives in an assisted living facility so she can receive the level of care she needs.

Even though Sandy’s parents built a solid retirement fund, it will only last another 12 to 18 months at the rate they’re currently paying for her mom’s care.

Gary’s advice to Sandy and others like her is that a parents’ LTC coverage is an investment in your future as much as it is your parents’. "It’s basically an estate-planning tool to prevent spending down your own retirement savings to take care of mom and dad in the nursing home," he explained. "We hope it’s something you never need, but it’s better to pay $300 a month for LTC than spend $60,000 a year for the next 10–15 years for nursing home care."

"I’m seeing firsthand what happens when the money runs out—even when you’ve planned," Sandy said. "My husband and I are working with an investment professional to give us direction now. I am thankful we started early to save regularly for retirement."

Times May Be Tough, but They Can Also Be Rewarding

Sometimes a parent’s financial challenges end up being a blessing for the entire family. As a single mom, Krystle M.’s mother was never able to build up much of a nest egg. But when Krystle, her husband and their two kids moved from Pennsylvania to South Carolina, they invited her mom to come with them.

"We were fortunate enough to have her move in with us," Krystle told us. "She watches our kids and helps out around the house. Essentially, she was able to retire when we moved, and it has taken a great burden off of her."

Though Lori W. and her husband never had a large income, they were debt-free. That gave them the flexibility to give her parents what they needed and keep their own retirement savings on track.

When health issues made it impossible for Lori’s mom and dad to live on their own, Lori took it upon herself to care for her aging parents financially and physically. "For the last three-and-a-half years, we cooked three meals a day and were on call 24 hours a day," she told us. "We did our best, and now that they have both passed away, we have peace knowing we did what was right for my parents."

Keep Your Retirement on Track by Working With a Pro

In the end, there’s no magical solution that will make supporting your parents in retirement a piece of cake. But with a lot of communication and teamwork, a commitment to stick to your own retirement plan, and a relationship with an investing professional, you and your parents can find the silver linings in this challenging time—and maybe even discover a way to appreciate this new chapter in your relationship.

Are you looking for a qualified investing pro? With a client-first mentality, our network of SmartVestor Pros can help you think long-term. They can educate and empower you to reach your retirement goals, and you can rest assured that your SmartVestor Pro cares as much about your financial future as you do!

Make an Investment Plan With a Pro

SmartVestor shows you up to five investing professionals in your area for free. No commitments, no hidden fees.

This article provides general guidelines about investing topics. Your situation may be unique. If you have questions, connect with a SmartVestor Pro. Ramsey Solutions is a paid, non-client promoter of participating Pros.

Did you find this article helpful? Share it!

About the author

Ramsey