Think that hefty tax refund you got last year was basically a big bonus? Think again.

A big, fat refund just means you’ve been loaning the government too much of your hard-earned cash with each paycheck, and Uncle Sam is simply returning money that was yours to begin with—that’s why it’s called a refund! It’s not a gift, and it’s definitely not free money!

Or maybe you have the opposite problem. You’re getting hit with massive tax bills, and you’re sick and tired of sending the IRS a big check every April. If that’s you, we feel your pain.

So how much should you withhold in taxes? And when should you withhold an additional amount from each paycheck?

Answering these questions is easier than you may expect, and it all starts with taking a closer look at your tax withholding.

Tax Withholding Explained

How do you avoid paying too much in taxes each month so you don’t get a big refund? You adjust your withholdings.

Every time you get a paycheck, your employer withholds taxes to send to the IRS. And you thought tax time was only in April? Nope. You pay taxes all year long through tax withholding.

When tax time rolls around, that’s when you find out if you had too much or not enough taxes withheld from your paycheck. Withheld too much? You’ll get a tax refund. Withheld too little? You’ll have to cut a check to the IRS. No thanks!

You really want to have a refund as close to $0 as possible without having to pay additional taxes. Yep, zero is a winning score when it comes to tax refunds, because who wants to loan the government their money for free? We want that money working for you, especially if you’re working the Baby Steps and kicking debt to the curb!

Understanding the New W-4 Form

Remember the first day of your job? Don’t worry. We don’t either. A new job is a blur of new names and spaces. But at some point, you probably filled out a W-4 form to help your employer figure out how much taxes to withhold from each paycheck.

The official government title for a W-4 is Employee’s Withholding Certificate, which sounds kind of fancy. But it’s not. You won’t hang this certificate in a place of honor next to the one you got for second place in a hot dog eating contest.

The W-4 is divided into five, fairly easy steps that will give your employer the info they need to calculate your withholding. Leave it to the government to label a five-step form with the number four! Here’s a rundown on the five steps you’ll see on a W-4:

- Step 1: You’ll enter some basic personal information here—name, address, Social Security number and filing status (single, married, head of household, etc.). Everyone has to fill out this step, but you only have to fill out steps 2–4 if they apply to you.

- Step 2: If you have more than one job, or you’re married filing jointly and your spouse also works, fill out this step. You’ll indicate exactly how many extra jobs you (or your spouse) have and information about your wages.

- Step 3: This is where you claim dependent tax credits to lower your taxes. Kids under 17 are $2,000 a pop. Other dependents are $500 each. Just a note here: The child tax credit was temporarily increased from $2,000 to a maximum of $3,600 per child in 2021 as part of the American Rescue Plan, and many taxpayers received advanced monthly payments. It reverted back to $2,000 in 2022.1

- Step 4: Here’s where you can make even more adjustments to your withholding for additional income (such as retirement income or self-employment income), deductions outside of the standard deduction, and any additional tax you want withheld from each paycheck.

- Step 5: Scribble your John Hancock on the dotted line, and you’re done!

The IRS introduced a new W-4 form in 2020. If you’ve been at your job for a while, you don’t have to fill out a new W-4 form. But it could be a good idea to check it anyway because the new form should help you get your tax withholding closer to where it needs to be.

Don’t settle for tax software with hidden fees or agendas. Use one that’s on your side—Ramsey SmartTax.

And besides, it’s always a good idea to do a “paycheck checkup” once in a while just to make sure your employer isn’t withholding too much (or too little) on payday.

Why Do You Need to Adjust Your Tax Withholding?

If you adjust your withholding so you break even (or get really close to breaking even) at tax time, you end up with more cash in your pocket throughout the year. In other words, you don’t send the IRS a big check, and you don’t get a huge refund back either.

IRS data shows that the average tax refund for the 2023 tax season was $2,812.2 So, let’s say you got paid twice a month and received the average refund. That means you should’ve had almost an extra $118 in every paycheck last year! Think of what you could do with $236 or more each month!

And if you went through a major life change over the past year that might impact how much you owe in taxes—you got married, bought a house, or welcomed a baby into the world—it’s a good idea to take a fresh look at your tax withholding and make any adjustments.

How to Calculate and Adjust Your Tax Withholding

So how do you figure out exactly how much you should be withholding from your paycheck so you don’t owe Uncle Sam a bunch of money or get a big refund? Good question! There are two simple ways to figure it out:

1. If nothing has changed in your tax situation: Take your refund amount or how much you owed from last year and divide it by 12. That’s how much you want to adjust your paycheck each month (divide by 24 if you’re paid twice a month).

2. If your tax situation has changed: Use tax software to do a fake tax return (you don’t have to pay anything if you don’t actually file the return). It will help you figure out if you’re paying too much (or too little). Then you can do that quick paycheck math again.

That’s two quick and easy options to calculate your withholdings. But let’s break it down step by step and answer some of those burning questions you might have:

Step 1: Total Up Your Tax Withholding

Let’s start by adding up your expected tax withholding for the year. You can find the amount of federal income tax withheld on your paycheck stub. Ugh, we know. It’s been years since you’ve looked at your paystub, and you don’t even remember how to log in to your payroll system. But this will be worth it!

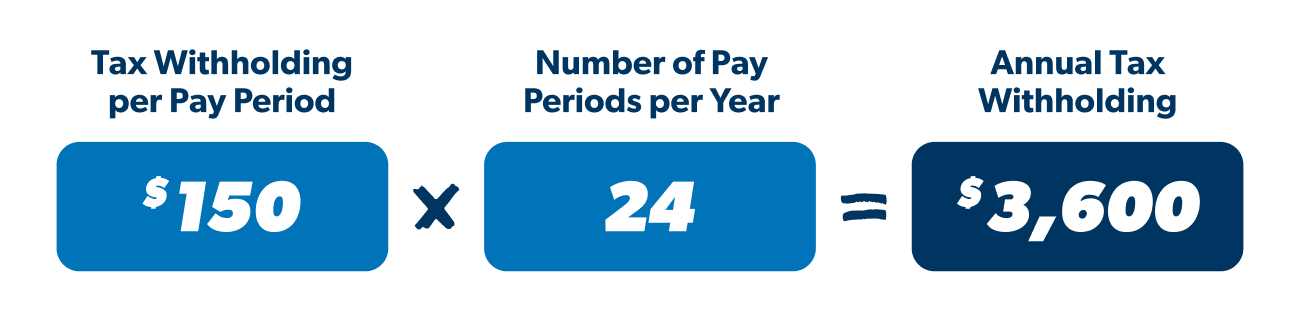

Let’s say you have $150 withheld each pay period and get paid twice a month. That would be $3,600 in taxes withheld each year.

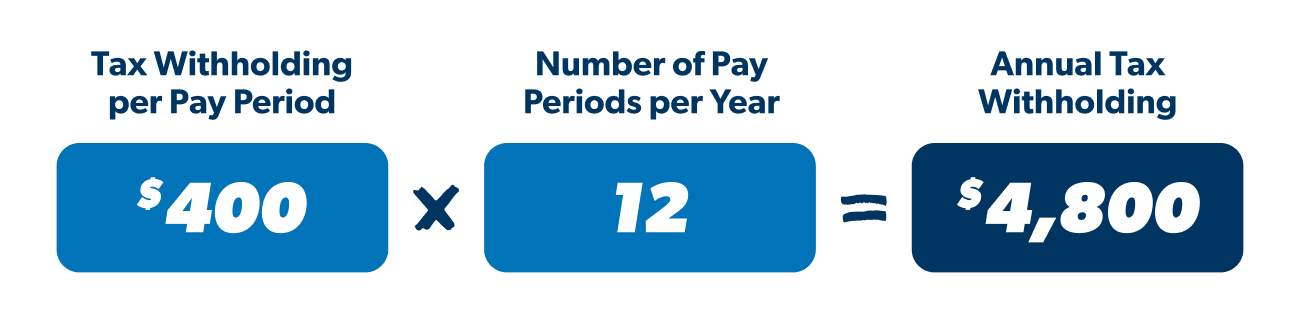

If you’re single, this is pretty easy. If you’re married filing jointly and both of you work, calculate your spouse’s tax withholding too. In this example, we’ll assume your spouse has $400 withheld each pay period and receives a monthly paycheck.

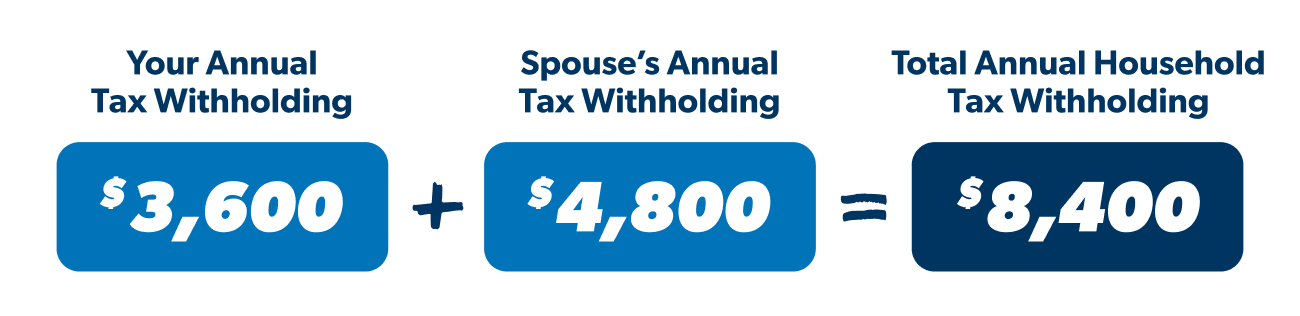

Then add the two together to get your total household tax withholding.

Step 2: Estimate Your Tax Liability

Now that you know your projected withholding, the next step is to estimate how much you’ll owe in taxes for this year.

The IRS provides worksheets to walk you through the process, which is basically like completing a pretend tax return.

If you’re married and filing jointly, for example, and your taxable income is around $81,500 for the 2023 tax year (after deductions), that puts you in the 12% tax bracket.3 But you actually won’t pay 12% on your entire income because the United States has a progressive tax system. Here’s how it breaks down:

- You’ll pay 10% on your first $22,000, which is $2,200.

- You’ll pay 12% on your next $59,500 ($81,500 - $22,000), which is $7,140.

- So $2,200 + $7,140 = $9,340. This is your tax liability.

Remember, federal taxes aren’t automatically deducted from self-employment income. If you have a side business or do freelance work, it’s especially important to factor that income into your tax equation to make sure you don’t end up with a big tax bill at the end of the year.

Step 3: Subtract the Difference

Once you have an idea of how much you owe the IRS, it’s time to compare that amount to your total withholding. Take your annual tax withholding and subtract your estimated tax liability.

Let’s continue our example from above and assume your estimated tax liability is about $9,300. In that case, you’d have a potential $900 deficit.

A positive balance indicates a refund, while a negative balance means you owe more and may have to pay the IRS interest and a penalty for underpaying your taxes. The good news is, you can fix it before tax time ever rolls around!

Step 4: Adjust Your Withholding

If you run the numbers and find you’ve got ground to make up, it’s best to adjust your tax withholding as quickly as you can. The longer you wait, the harder it’ll be to get it just right. You have two options:

- File a new W-4 and submit it to your employer. If you’ve been at your job for a while and you’ve been getting big refunds or tax bills for years, filling out a new W-4 could help you get your tax withholding right.

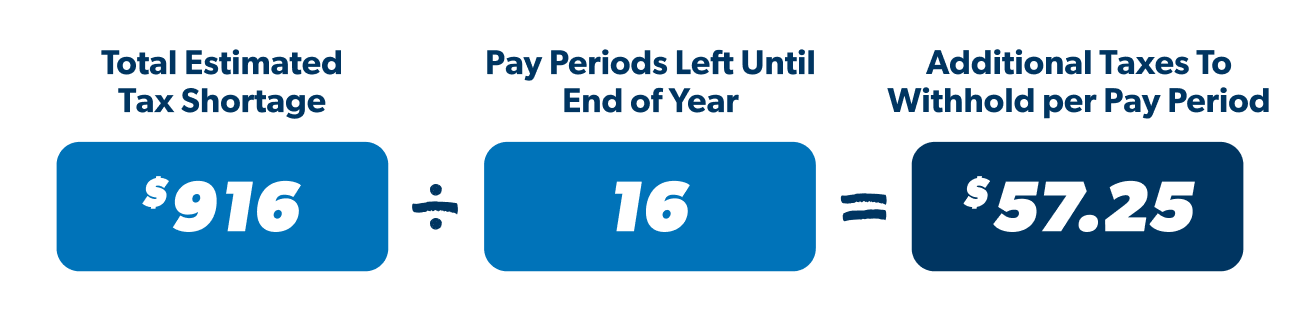

- Specify additional withholding. As mentioned above, you have the option on the W-4 form to enter an additional amount you want to have withheld with each paycheck. Simply divide your estimated tax shortage by the number of pay periods you have left before the end of the year to get your number.

Do Taxes the Right Way

If you get stuck along the way or don’t feel comfortable with your numbers, ask a RamseyTrusted tax pro for help. They’re experts when it comes to taxes. They can make sense of your personal tax situation and guide you toward a reasonable target.

With a few minor adjustments, you can strike a better balance and look toward next year’s tax season with a lot less stress. (Okay, maybe saying you’ll “look forward” to tax season is a bit generous.)

If you’re ready to file your taxes online, check out Ramsey SmartTax. It’s tax software that’s easy to navigate and affordable, so you can file your return with confidence.

Federal Classic Includes:

-

All major income types and federal forms

-

Prepare, print and e-file

-

Phone and email support

-

1 year of audit assistance

Federal Premium Includes:

Everything in Classic plus:

-

Live chat

-

Priority phone and email help

-

Free financial coaching session

-

3 years of audit assistance

Did you find this article helpful? Share it!

About the author

George Kamel