Do you have mortgage questions? You aren’t alone.

Mortgages can be complicated, but it’s important to understand your options. Knowing the answers to your mortgage questions can empower you to make smart decisions, whether you’re buying your first home or interested in refinancing your current mortgage.

Common Mortgage Questions

Learning about your different mortgage options before you meet with a lender can help you get the best deal on a house that will benefit your family for years to come.

Here are some common mortgage questions you may have during the home-buying or refinancing process.

1. How do you qualify for a loan?

The idea of meeting with a lender can be intimidating, especially if you’re buying your first home. After all, this is probably the biggest purchase you’ll ever make!

Take a deep breath and relax—you don’t have to be stressed. Think of your first meeting with a lender as a get-to-know-you session. They’ll simply want to learn a few basics about you and your financial situation.

Then comes the paperwork! Once your loan process gets started, be prepared to provide proof of:

- Where you work

- Your income

- Any debt you have

- Your assets

- How much you plan to put down on your home

A good lender will clearly explain your mortgage options and answer all your questions so you feel confident in your decision. If they don’t, find a new lender. A mortgage is a huge financial commitment, and you should never sign up for something you don’t understand!

It’s likely that your lender will approve you for more money than you want to spend. But keep this in mind: Just because you qualify for a big loan doesn’t mean you can afford it!

If you are you ready to get prequalified for a mortgage loan, we recommend talking with Churchill Mortgage.

Just because you qualify for a big loan doesn’t mean you can afford it!

2. Can you get a mortgage without a credit score?

This is one of the most commonly asked mortgage questions, and the answer may surprise you.

If you’ve paid off all your debt—and we recommend you do before buying a home—it is possible you won’t have a credit score when you meet with a lender. That might make you nervous. But don’t worry; you can still get a mortgage.

If you apply for a mortgage without a credit score, you’ll need to go through a process called manual underwriting. Manual underwriting simply means you’ll be asked to provide additional paperwork for the underwriter to review personally. Your loan process may take a little longer, but buying a home without the strain of extra debt is worth it!

Not every lender offers manual underwriting. Do a little research on the front end to find the ones in your area that will, like Churchill Mortgage.

Get the right mortgage from a trusted lender.

Whether you’re buying or refinancing, you can trust Churchill Mortgage to help you choose the best mortgage with a locked-in rate.

3. What’s the difference between being prequalified and preapproved?

A quick conversation with your lender about your income, assets and down payment is all it takes to get prequalified. But if you want to get preapproved, your lender will need to verify your financial information and submit your loan for preliminary underwriting. A preapproval takes a little more time and documentation, but it also carries a lot more weight.

A preapproval takes a little more time and documentation, but it also carries a lot more weight.

Which is better? Think of prequalification as an initial step and preapproval as the green light signaling that you’re ready to start your home search. When sellers review your offer, a preapproval means you’re a serious buyer whose lender has already started the loan process.

4. How much home can you afford?

Buying "too much house" can quickly turn your home into a liability instead of an asset. That’s why it’s important to know what you can afford before you ever start looking at homes with your real estate agent.

Buying too much house can quickly turn your home into a liability instead of an asset.

We recommend keeping your monthly mortgage payment to 25% or less of your monthly take-home pay. For example, if you bring home $5,000 a month, your monthly mortgage payment should be no more than $1,250. Using our easy mortgage calculator, you’ll find that means you can afford a $211,000 home on a 15-year fixed-rate loan with a 20% down payment.

Dave Ramsey recommends one mortgage company. This one!

With a conservative monthly mortgage payment, you’ll have room in your budget to cover additional costs of homeownership, like repairs and maintenance, while saving for other financial goals, including retirement.

5. How much should you save for a down payment?

We recommend putting at least 10% down on a home, but 20% is even better because you won’t have to pay private mortgage insurance (PMI). PMI is an extra cost added to your monthly payment that doesn’t go toward paying off your mortgage.

Saving a big down payment takes hard work and patience, but it’s worth it. Here’s why:

- You’ll have built-in equity when you move into your home.

- You can finance less, which means you’ll have a lower monthly payment.

On the flip side, if you buy a home with little to no down payment and the market dips, you could be stuck until home values recover.

If the goal is to pay off your home quickly, why not get a head start with a big down payment? Now that’s a good game plan!

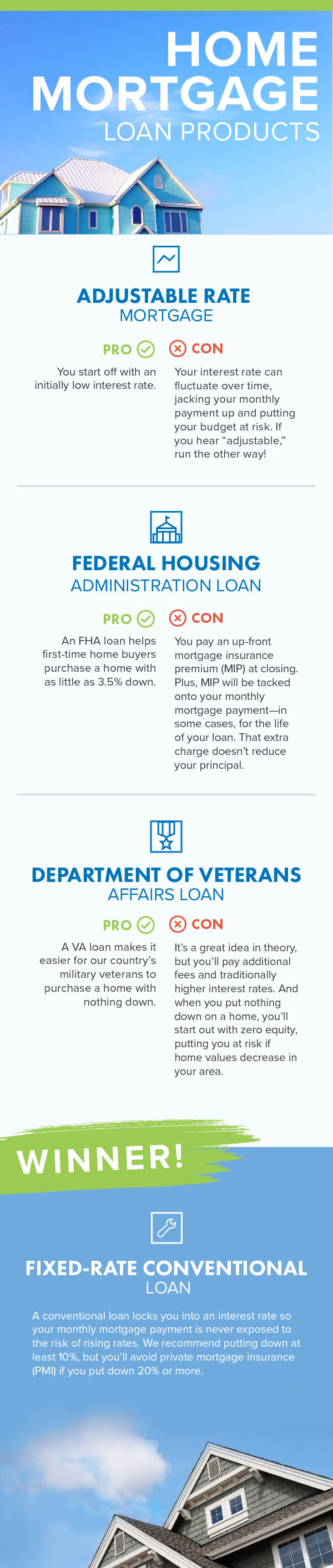

6. How do you know which home mortgage option is right for you?

With so many mortgage options out there, it can be hard to know how each would impact you in the long run. Here are the most common mortgage loan types:

- Adjustable-Rate Mortgage (ARM)

- Federal Housing Administration (FHA) Loan

- Department of Veterans Affairs (VA) Loan

- Fixed-Rate Conventional Loan

We recommend choosing a 15-year fixed-rate conventional loan. Why not a 30-year mortgage? Because you’ll pay thousands more in interest if you go with a 30-year mortgage. For a $250,000 loan, that could mean a difference of more than $100,000!

A 15-year term does come with a higher monthly payment, so you may need to adjust your home-buying budget to get your mortgage payment down to 25% or less of your monthly income.

But the good news is a 15-year mortgage actually pays off in 15 years. Why be in debt for 30 years when you can knock out your mortgage in half the time and save six figures in interest? That's a win-win!

Why be in debt for 30 years when you can knock out your mortgage in half the time and save six figures in interest?

7. How do interest rates affect your mortgage?

High interest rates bring higher monthly payments and increase the overall interest you’ll pay over the life of your loan. A low interest rate saves you money in both the short and long term.

Of course, just like you can’t time the stock market, it’s nearly impossible to time your home purchase with the best interest rates. The past five years have held some of the most affordable interest rates ever, according to the Federal Home Loan Mortgage Corporation, and their recent forecast predicts the trend will continue.1

It may be hard to time your home purchase with the best interest rates, but there are things you can do to get a lower rate. For example, a benefit of the 15-year, fixed mortgage is that it has a lower interest rate than a 30-year, fixed mortgage. Sometimes a bigger down payment can also help you get a better interest rate.

The money you pay in interest doesn’t ever go toward paying off the principal balance of your home. That’s why it’s a smart move to get a low interest rate on your mortgage and then pay off your house as quickly as you can.

8. How do you lock your interest rate?

Because mortgage interest rates can change day to day, locking your rate is an important part of the mortgage process. Locking your interest rate guarantees a certain interest rate for a specific period of time, usually between 30 and 60 days.

In most cases, you can lock your interest rate as soon as your initial loan is approved. However, most buyers wait until they have found a specific home to purchase and are officially under contract.

Like we said earlier, mortgage interest rates go up and down and there’s no way to time it perfectly. You simply don’t know what the future holds. No one does. So don’t spend time trying to time the market; instead, rely on your lender’s expertise. If they say it’s a good time to lock down your rate, trust them.

Some lenders charge a fee to lock your interest rate. Ask questions on the front end so you know what to expect.

9. What are mortgage points?

Mortgage points, or discount points, are a way to prepay interest to get a lower interest rate on your mortgage.

Each mortgage point equals 1% of your home’s value. That means if you’re getting a $250,000 loan and have two discount points, you’ll pay $5,000. In most cases, a point can reduce your interest rate by one-eighth to one-quarter of a percent.

We don’t recommend discount points because of how long it takes to break even on that cost. In most cases, you’ll sell your house or could even pay it off before you recoup the money you paid up front in points. Skip the points and focus on putting as much money into your down payment as you can.

You should also avoid paying for other types of mortgage interest rate buydowns, like a 3-2-1 buydown.

10. What does your mortgage payment include?

So what happens when you send in that mortgage payment every month? It’s nice to think the whole amount just reduces your principal, but your monthly payment actually goes toward a lot more.

Here’s what the typical monthly mortgage payment includes:

- Principal

- Interest

- Homeowners insurance

- Property taxes

- Private mortgage insurance (PMI), if you put down less than 20% on your home

If you want to pay more on your mortgage, be sure to specify that you want any extra money to go toward the principal only, not an advance payment that prepays interest.

If you want to pay more on your mortgage, be sure to specify that you want any extra money to go toward the principal only, not an advance payment that prepays interest.

11. What is an escrow account, and how does it work?

Your mortgage payment may include additional costs like your homeowner’s insurance and property taxes. These are annual expenses that are part of homeownership, and the lender is at risk if you don’t make those payments.

Your lender can add the monthly portion of each of those accounts to your mortgage payment. That money is held in an escrow account that is managed by a third party to make sure those costs are paid on time.

12. When should I consider refinancing?

You should definitely think about refinancing if:

- You can lower your interest rate enough to justify the closing costs.

- You can refinance from an adjustable-rate mortgage to a fixed-rate mortgage.

It’s probably not worth it to refinance if you could lower your interest rate by half a percent. But let’s say it’s going to take another eight years for you to pay off your house and you could lower your interest rate from 6% to 4%.

On a $200,000 mortgage, lowering your interest rate from 6% to 4% could save you about $200 a month. Over the course of eight years, that adds up to more than $19,000. Closing costs to refinance a $200,000 loan cost an average of $2,000.3 Is it worth it to pay $2,000 in closing costs to save $19,000 over the long term? Probably so!

When it comes to adjustable-rate mortgages, refinancing to a fixed-rate mortgage is almost always a good idea. An adjustable-rate mortgage can go up and down, drastically changing your monthly payment. That’s not a risk we want you to take. A fixed-rate mortgage is your best option, even if you have to write a check for the closing costs.

Don’t refinance to anything longer than a 15-year, fixed-rate mortgage. Remember, the goal of refinancing is to pay off your house faster, not stay in debt longer!

If you already have a good interest rate on a 30-year, fixed loan, you don’t have to refinance just to get a shorter term. It’s easy to pay extra on your mortgage. Our mortgage payoff calculator can help you estimate how much extra you need to pay every month to hit your goal.

13. What happens after you get preapproved for a home mortgage loan?

Getting preapproved for a mortgage is just the beginning. Once the financial pieces are in place, it’s time to find your perfect home! While it’s one of the most exciting stages of the process, it can also be the most stressful. That’s why it’s important to partner with a buyer’s agent.

A buyer’s agent can guide you through the process of finding a home, negotiating the contract, and closing on your new place. The best part? Working with a buyer’s agent doesn’t cost you a thing! That’s because, in most cases, the seller pays the agent’s commission.

Why not partner with a real estate pro who can save you time, stress and money on your home purchase? We can connect you with a high-octane real estate agent in your area who’s earned our seal of trust.

14. How long does it take to close on a house?

The average time to close on a house is currently around 40 days.4 Factors such as your loan type, your financial situation, and the length of your contract can either lengthen or shorten that time frame.

15. What happens at closing?

When you close, that new house and mortgage are officially yours. At the closing, you’ll sit down with the professionals involved in your real estate transaction and sign all the legal documents needed to give you ownership of your new place. That’s pretty exciting!

You’ll also be responsible for paying closing costs as part of the closing process. Closing costs are typically 3–4% of your home’s purchase price. You’ll receive a Closing Disclosure three days before closing so you know exactly what you can expect.

If you have questions about the closing process, talk to your real estate agent or lender.

Have more questions about mortgages? Talk to a real estate agent!

An experienced real estate agent can answer any mortgage questions you may have. Imagine looking back 10 years from now, knowing you made a smart home purchase that kept your financial goals on track! Wouldn’t that be a relief?

It’s time to turn your home-buying dream into reality by partnering with a real estate expert.

Considering refinancing? Talk to Churchill Mortgage!

Did you find this article helpful? Share it!

About the author

Ramsey