Here’s something you may not have thought about when you celebrated your 40th birthday: You’re about as close to traditional retirement age as you are to your high school graduation. Feeling old yet?

If that thought stirs a bit of fear in your heart, you’re not alone. The Employee Benefits Research Institute reports that 11% of all employees age 35–44 and 14% of employees age 45–54 have less than $1,000 saved for retirement.1 If you’re one of those folks, there should be all kinds of alarms going off in your head. This is your wake-up call!

We’re not going to beat around the bush here: You’ve got your work cut out for you if you want to be a millionaire. But don’t give up hope! Even if you’re 40 years old with nothing saved for retirement, not only is it possible to build a $1 million nest egg by the time you reach your golden years—it might not be as hard as you think to get there.

There Is Still Time to Become a Millionaire

Here’s the best news about being in your 40s: You’re smack dab in the middle of your prime earning years, which is when most workers earn their highest annual incomes. All that hard work you did in your 20s and 30s to get your career off the ground is starting to pay off—literally!

According to the U.S. Census Bureau, the typical household income for those between ages 35–44 is $85,694. The only age group with a higher household income are folks who are 45 to 54 years old ($90,359).2 So if you’ve dug yourself into a hole when it comes to saving for retirement, you at least have a larger shovel to dig yourself out!

Let’s say you just turned 40 and realized, Oh crap! I have nothing saved for retirement! What do you do? Whether you’re 24 or 42, the Baby Steps are still the quickest right way to build wealth and become a millionaire. Here’s how.

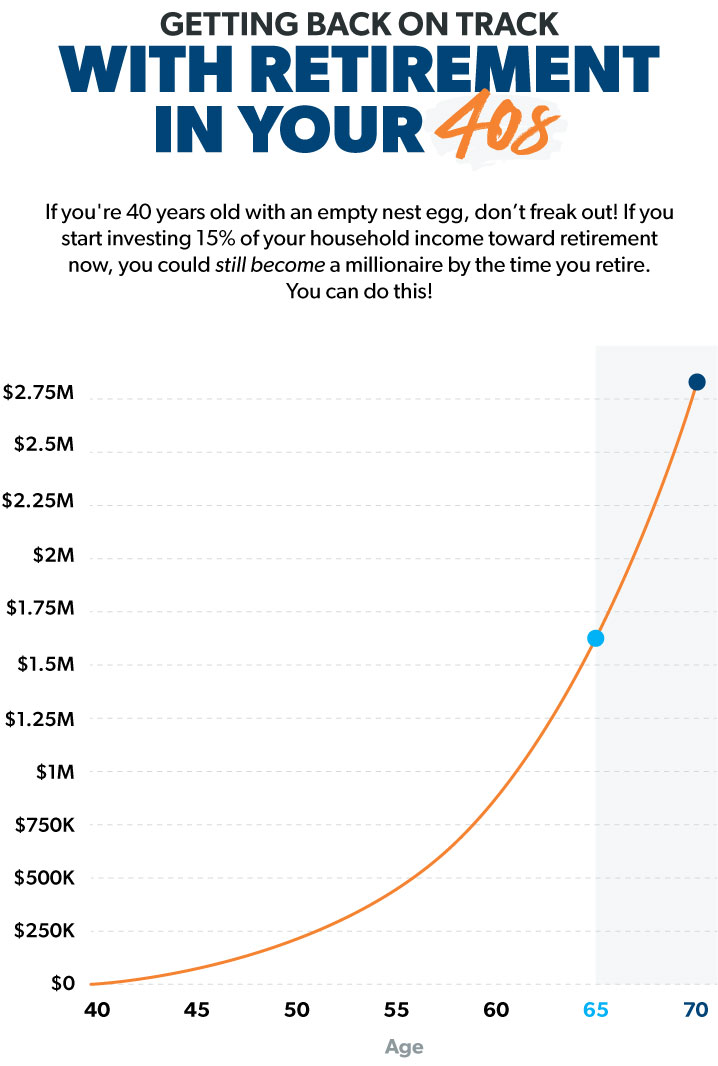

Once you’re debt-free with a fully funded emergency fund in place, it’s time to put the pedal to the metal and start investing for retirement (Baby Step 4). How much do you need to save? You need to invest at least 15% of your gross income for retirement. No exceptions!

So if you’re 40 years old and your household income is $80,000, that means you should be investing $1,000 each month into retirement. Whether it’s cutting out that daily trip to Starbucks or saying goodbye to cable, do whatever you have to do to make room in your budget for those retirement savings. This is your future we’re talking about here!

If you invest that money in good growth stock mutual funds, you could have more than $1.5 million saved in your retirement nest egg by the time you’re 65 years old. And if you held off retirement for another five years after that, you could retire at age 70 with $2.8 million!

You see? It is possible to retire a millionaire—even with a late start. But you need to get started today!

How You Can Get Back on Track With Retirement Savings

So now that you know it’s possible to reach your $1 million retirement goal, you’re probably wondering if you can afford to invest that much of your income each month to reach that goal. The real question is: Can you afford not to?

How much will you need for retirement? Find out with this free tool!

Here are some tips that will help get you back in the game and on track for a million-dollar nest egg. Will it be easy? No! It’s going to take hard work. It’s going to take some sacrifices. But guess what? The peace that comes with having a nest egg that will allow you to retire with dignity is worth it every single time.

1. Take advantage of your 401(k).

Where should you put your money to get the most bang for your buck? The easiest and often most effective way to get started is through your workplace retirement plan like a 401(k). In fact, 8 out of 10 millionaires invested in their company’s 401(k) plan, according to The National Study of Millionaires.

Most employers who offer a 401(k) will match a portion of your investment, so invest enough to get the full match for an instant and guaranteed 100% return on your money!

If your employer offers a Roth 401(k) option and the plan offers a choice of good growth stock mutual funds, you can invest the entire amount in your workplace plan. If a Roth 401(k) isn’t available, simply invest up to the employer match in your 401(k) then open a separate Roth IRA to invest the remainder.

Make an Investment Plan With a Pro

SmartVestor shows you up to five investing professionals in your area for free. No commitments, no hidden fees.

Ramsey Solutions is a paid, non-client promoter of participating pros.

2. Get debt out of your life—forever!

Trying to save for retirement while you’re juggling credit card, student loan and car payments is like trying to climb Mount Everest with a backpack full of bricks—you’re not going to get very far!

A recent study shows that about 30% of Americans’ monthly income goes to paying off consumer debt.3 How in the world are you supposed to save for retirement when about one-third of your income is going to banks and lenders every month? Spoiler alert: You can’t!

Do you know what you’ll have if you don’t have any debt payments? Money! If you have debt, your top priority is to get out of it as quickly as possible. Set retirement saving aside for now. Budget for the basics, then tackle your debt using the debt snowball method.

Once you’re out of debt except for your home and have a fully funded emergency fund (3–6 months of expenses) then yes, you can afford to invest 15% or more of your income each month for retirement.

3. Make saving for retirement a priority in your budget.

If you don’t plan your spending each month, it’s easy to feel like you’re broke all the time. Isn’t that why you’re behind on retirement savings now? A budget allows you to set your spending priorities before the month begins, so you always know where your money’s going and how it’s working for you.

When you sit down to make a budget, you should plan in this order: give, save, spend. Here’s what that looks like:

- First, set aside some of your income for giving. We believe you should give 10% no matter where you are on your financial journey. After all, giving is the most fun you will ever have with money, and you can’t put a price tag on having a spirit of generosity!

- Second, you should budget for your savings goals. If you’re on Baby Step 4, that includes investing 15% for retirement!

- After that, you can move on to budgeting for monthly expenses. Start with the essentials (like food, shelter, utilities and transportation) before moving on to any nonessentials (like fun money and entertainment).

- Pro tip: When you subtract all your expenses (giving, saving and spending) from your income, it should equal zero. That’s what we call a zero-based budget, and that’s a good thing! It means you’ve given every dollar an assignment. Good job!

When you regularly make generosity and saving a part of your life, eventually it becomes a habit that gets easier and easier over time. You might have to cut back on some things like eating out or traveling to make room for retirement savings. But making that sacrifice now means you won’t be sweating bullets by the time you want to retire.

You may have let the previous 20 years of your career roll by without getting serious about retirement savings, but that doesn’t mean you have to spend the next 20 years the same way. Change your habits now, get on a plan, and change your future for the better!

Next Steps

- Use our R:IQ Retirement Assessment to find out how much money you may need to retire based on your situation.

- Grab a copy of Dave Ramsey’s book Baby Steps Millionaires and learn how to bust through the barriers preventing you from becoming a millionaire.

- Talk with a financial advisor who will help you choose your investments, keep an eye on their performance, and keep you focused on your plan.

This article provides general guidelines about investing topics. Your situation may be unique. If you have questions, connect with a SmartVestor Pro. Ramsey Solutions is a paid, non-client promoter of participating Pros.

Did you find this article helpful? Share it!

About the author

Ramsey